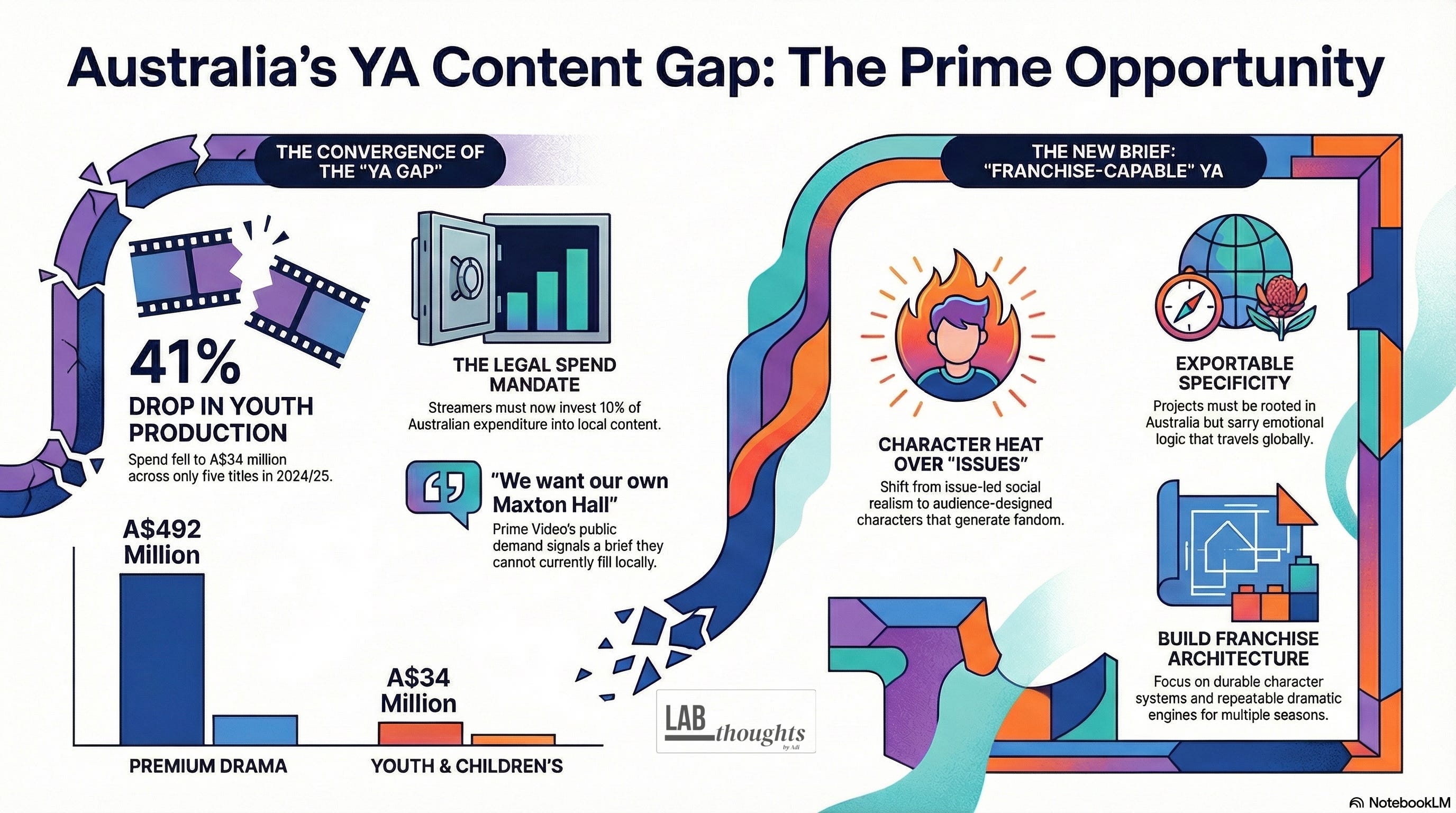

TL;DR: In March, Prime Video Australia said publicly it wants its own Maxton Hall or The Summer I Turned Pretty. Screen Australia’s 2024/25 drama data shows youth and children’s production collapsed 41% in a single year, to A$34 million across five titles, while premium drama narrowed on volume and jumped 44% in average cost per hour. Australia’s new streaming quota obligations mean the major platforms now have a legal requirement to put local content spend somewhere. A named category, measurable underproduction, and mandatory spend pressure are three separate things that rarely line up. They are lining up now.

Prime Video Australia said it wants its own Maxton Hall or The Summer I Turned Pretty That line came out of a Prime Video Australia and New Zealand slate event in March. It has not been treated as a major story. It should be.

A platform does not name specific global franchises in public unless it has a brief it cannot fill locally.

Maxton Hall is a German-language adaptation of a YA novel that became one of Prime Video’s most-watched non-English originals globally in 2024. The Summer I Turned Pretty is a US YA franchise now in its third season, built on character heat, audience attachment, and reliable repeat viewing. These are not vague taste references. They are category specifications.

That quote is not an aspiration. I think it is a gap admission.

Australia has the talent, the stories, and now the policy environment to answer it. What it does not have is a reliable pipeline of commercially legible YA with real franchise legs.

That is the gap. The Prime signal just made it harder to pretend otherwise.

What the gap actually is

Commercially legible YA is a specific category. It is not children’s drama. It is not prestige drama with younger faces. It is not issue-led social realism with a teenage protagonist. Those things exist and they serve real purposes, but none of them is the same category and none of them answers the brief.

Commercially legible YA is audience-designed franchise IP. Stories with character heat strong enough to generate fandom, not just viewership. Emotional repeatability. Readable desire. A reason to come back for season two that is not “the story continues” but “I need to know what happens to these specific people.” Discoverable through recommendation systems and social conversation. Portable enough to travel beyond the home market without losing what made it specific to begin with.

Australia produces isolated examples of this. It does not produce a consistent pipeline.

The local market has tended to treat the gap as a cultural problem, a matter of creative courage or institutional risk appetite. It is also a structural problem. The category has not been built with the same deliberateness that premium drama has. The infrastructure around it, the development funding, the commissioning language, the producer expertise in franchise design and audience architecture, remains thin.

Prime’s stated preference is a prompt to take the structural problem seriously.

What the numbers show

The Screen Australia Drama Report 2024/25 makes the production economics visible.

Premium drama is narrowing. Subscription TV and SVOD drama spend rose to A$492 million across the year, but concentrated into only 18 titles. Average budget per hour jumped 44% to A$5.1 million. The lane still exists and it is well-funded. It is also getting more expensive to enter and less likely to expand in volume.

Youth and children’s drama went in the other direction. Production spend fell to A$34 million, down 41% from the previous year, across only five titles. That is not a rounding error in a category trend. That is near-collapse in a single reporting period.

The middle lane, where commercially ambitious YA would logically sit, is not represented in those figures as a distinct category. That absence is itself information. It confirms that the market has not yet built the infrastructure to produce commercially legible YA at meaningful volume or consistency.

One way to read those numbers: premium drama is too expensive for most projects without major platform backing, and youth drama is underfunded and low-volume.

The category that could sit between them, franchise-capable YA with genuine audience design, has no home in the current production landscape.

Why the timing has changed

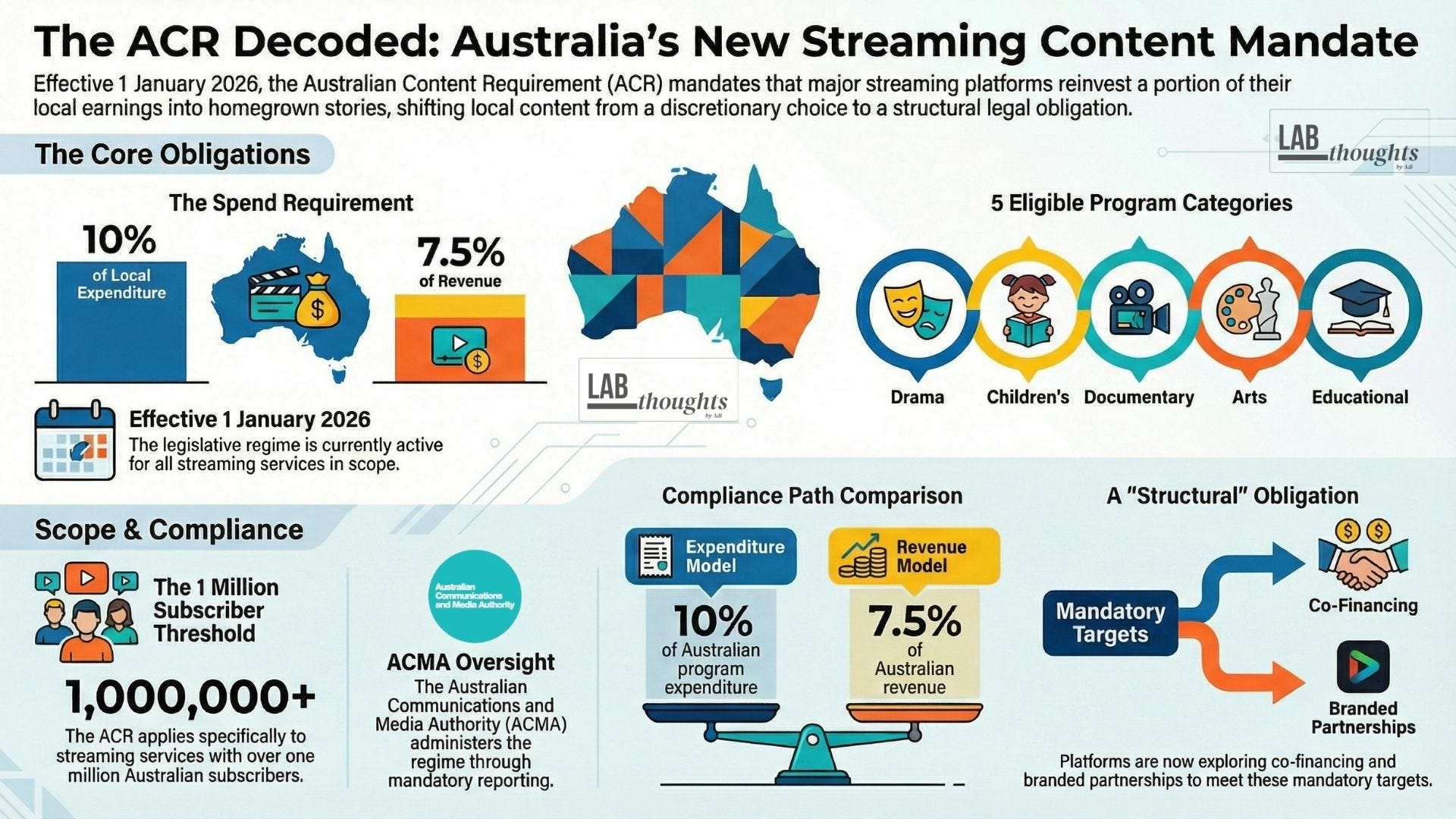

Australia’s streaming quota obligations changed the underlying maths.

The major services are now required to invest at least 10% of their Australian programme expenditure, or 7.5% of local revenue, into new local drama, children’s, documentary, and related content. The spend has to go somewhere.

The live question is not whether streamers need Australian content. They do, and they are legally required to fund it.

The more useful question is which categories are still underbuilt enough to become strategically important for a platform trying to deploy that spend well. A category where the platform has already said it wants more, where local production volume is demonstrably low, and where the global model for what success looks like has been established by titles the platform has named, is not a vague opportunity. It is a specific one.

The quota obligation and the Prime buyer signal are not related by coincidence. They are converging on the same gap at the same moment.

What Prime now wants from local content everywhere

Piece 1 of this series argued that Prime Video’s India showcase revealed how the platform now thinks about local content in any market. The operating brief, established through India’s multilingual, multi-window, multi-revenue-lever ecosystem, is that local content needs to carry multiple kinds of value at once: subscriber value, advertising value, franchise value, and export potential.

That brief applies here too. A project that can only justify its budget as a domestic SVOD original is a harder sell inside that model than it was three years ago. A project with franchise logic, audience elasticity, and cross-border emotional legibility is a better fit.

Read the Maxton Hall reference through that lens. That title worked because it was rooted in a specific place, a German boarding school backdrop, while carrying emotional logic that travelled cleanly.

Prime is not asking for something less Australian. It is asking for something Australian enough to be specific and legible enough to move.

What franchise-capable YA actually requires

The brief is more demanding than it first sounds.

Franchise-capable YA is not high concept. High concept is a logline strategy. Franchise capability is an audience design strategy. They are not the same.

The projects that develop genuine franchise legs have durable character systems. The audience forms an attachment to specific people, not just a plot. Strong audience identification: the viewer has a clear emotional access point, a character they are watching for, a relationship dynamic they are invested in.

A repeatable dramatic engine that can sustain more than one season without either repeating the first season’s structure or abandoning what made the audience care. Tonal control: the viewer knows what emotional return they are getting when they come back. And fandom logic, meaning the story generates conversation, investment, and social circulation between episodes and between seasons.

Prime has named its own models. Each one illustrates a different part of the mechanism.

Maxton Hall is the clearest buyer signal. It runs on a durable central pairing, a clean class-and-desire engine, and a school ecosystem with enough structural room to sustain conflict across seasons.

The Summer I Turned Pretty is the clearest Prime-owned model for emotional repeatability. Its real asset is not plot novelty. It is tonal control. The audience knows exactly what feeling it is returning for, and the show delivers it without apology.

Culpables sharpens the IP point. Romance-led youth material with enough intensity and audience attachment does not stay a one-off. It becomes a franchise system.

Australia has already proved one part of this equation. Heartbreak High (Netlfix) travelled because it was specific, noisy, contemporary, and character-led. It did not flatten its local voice to move. But it marks a distinction worth holding. It is the strongest local proof that Australian youth stories can travel. It is not quite the same thing as the cleaner romance-franchise lane Prime has now named.

Surviving Summer (Netflix) sits closer to that streaming-facing teen lane, and it is useful for exactly that reason. It shows that exportable setting, young cast, and platform-friendly readability are not enough on their own. Place can open the door. Character systems keep it open.

That is the bar. It is not the bar the Australian market typically sets for itself in this category.

The projects that miss it tend to share a few failure modes. An issue-led premise that treats the audience as a constituency rather than a group of people who want to feel something specific. A “youth” label applied to what is essentially a prestige drama with a younger cast. Tonal templates imported from American or British YA that flatten the local specificity that would make the project actually worth watching. Character dynamics designed for approval rather than attachment.

None of those is franchise-capable YA. And none of them is what Prime has said it wants.

A category gap in public

A major platform has named a category gap in public. The production data confirms the gap is real. The policy environment creates spend pressure that makes filling the gap more viable than it has been.

That is a more specific set of conditions than the Australian screen industry usually gets to work with. Most market signals are diffuse. This one is named, evidenced, and time-sensitive.

The question for producers and developers working in or adjacent to this category is not whether the opportunity is real. It is whether the projects in development are actually built to answer the brief, or whether they are built to answer an older, softer version of it.

Character heat. Fandom logic. Franchise architecture. Export legibility. Those are not aspirational descriptors for a pitch deck. They are the operating requirements.

The gap is there. The brief is clear. The work is in the build.

Sources

Jesse Whittock, “Prime Video Australia Seeks Its YA Moment As Deadloch Season 2 Nears,” Deadline, 13 March 2026.

Naman Ramachandran, “Prime Video Touts India as ‘Most Important’ Global Market,” Variety, March 2026.

Screen Australia Drama Report 2024/25.

Australian Government streaming quota announcement, November 2025.