TL;DR: Gen Z now makes up 39% of North American cinema audiences, up from 34% in 2019. In Australia, 14-24-year-olds are the most frequent cinemagoers and over-index versus their share of the population. Across APAC, the pattern holds in pieces: Indonesia, Thailand, Vietnam and Japan are all showing youth-driven theatrical momentum. But South Korea shows what happens when audience willingness meets a weak supply side. The lesson is not “Gen Z saves cinema.” It is that Gen Z rewards films that function as outings, not content.

I was on a train in Sydney recently and most of the carriage was watching something. Headphones in, phones out, algorithm fed. Individual, frictionless, free. Nobody was negotiating where to sit or what to see. Nobody was buying anything.

That image is the business problem in miniature. Not that young people do not watch screen content. They watch more than any generation before them. The problem is that most of that watching costs studios and exhibitors nothing and earns them nothing.

The battle for theatrical is not really about whether Gen Z likes cinema. It is about whether what you are making is good enough to pull them off the train and into a seat that costs money.

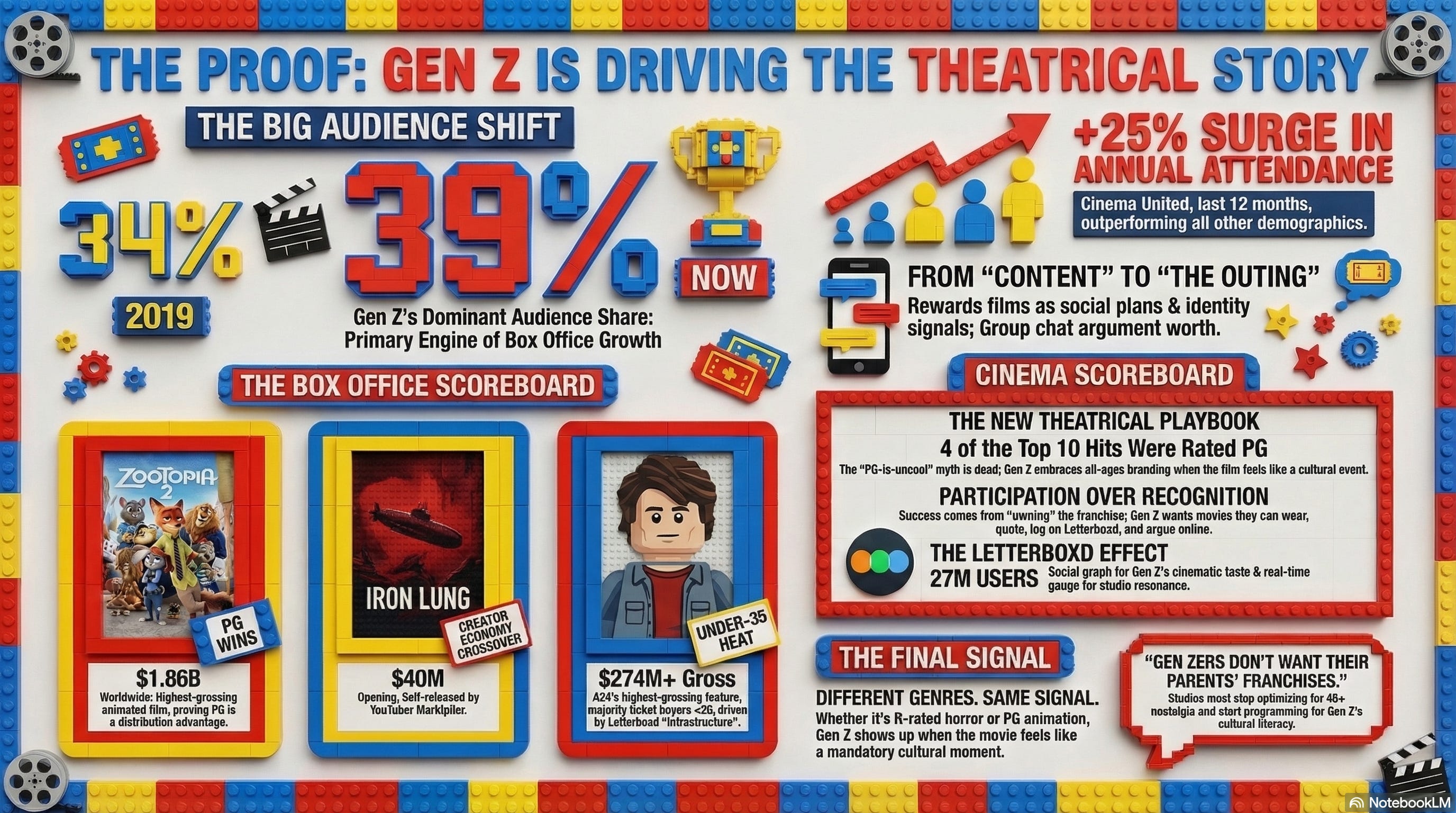

The Hollywood Reporter’s March 2026 feature on Gen Z and theatrical puts some useful numbers on the trend. Gen Z now represents 39% of the North American cinema audience, up from 34% in 2019.

Cinema United recorded a 25% rise in Gen Z attendance over the prior 12 months. Four of the top-grossing films of 2025 were rated PG.

Zootopia 2 became the highest-grossing animated film of all time at $1.86 billion worldwide. Iron Lung, self-released by YouTuber Markiplier, opened to $40 million. A24’s Marty Supreme, the Timothée Chalamet ping-pong film, became A24’s highest-grossing feature at over $274 million worldwide, with most of those ticket buyers under 35.

Now these are not flukes. They are pattern.

So come on, lets do what Labs Thoughts does…lets dig in.

What the hits have in common

It is not genre. PG animation, R-rated horror, arthouse caper films, and YouTuber vanity projects have almost nothing in common aesthetically. What they share is function.

Each of these films gave its audience something to do with the experience after it was over. A Letterboxd log. A fancam. A spoiler to avoid. A group chat argument. A meme that meant you were in on something.

The film was the outing and the content simultaneously. That is a different product from “a movie.”

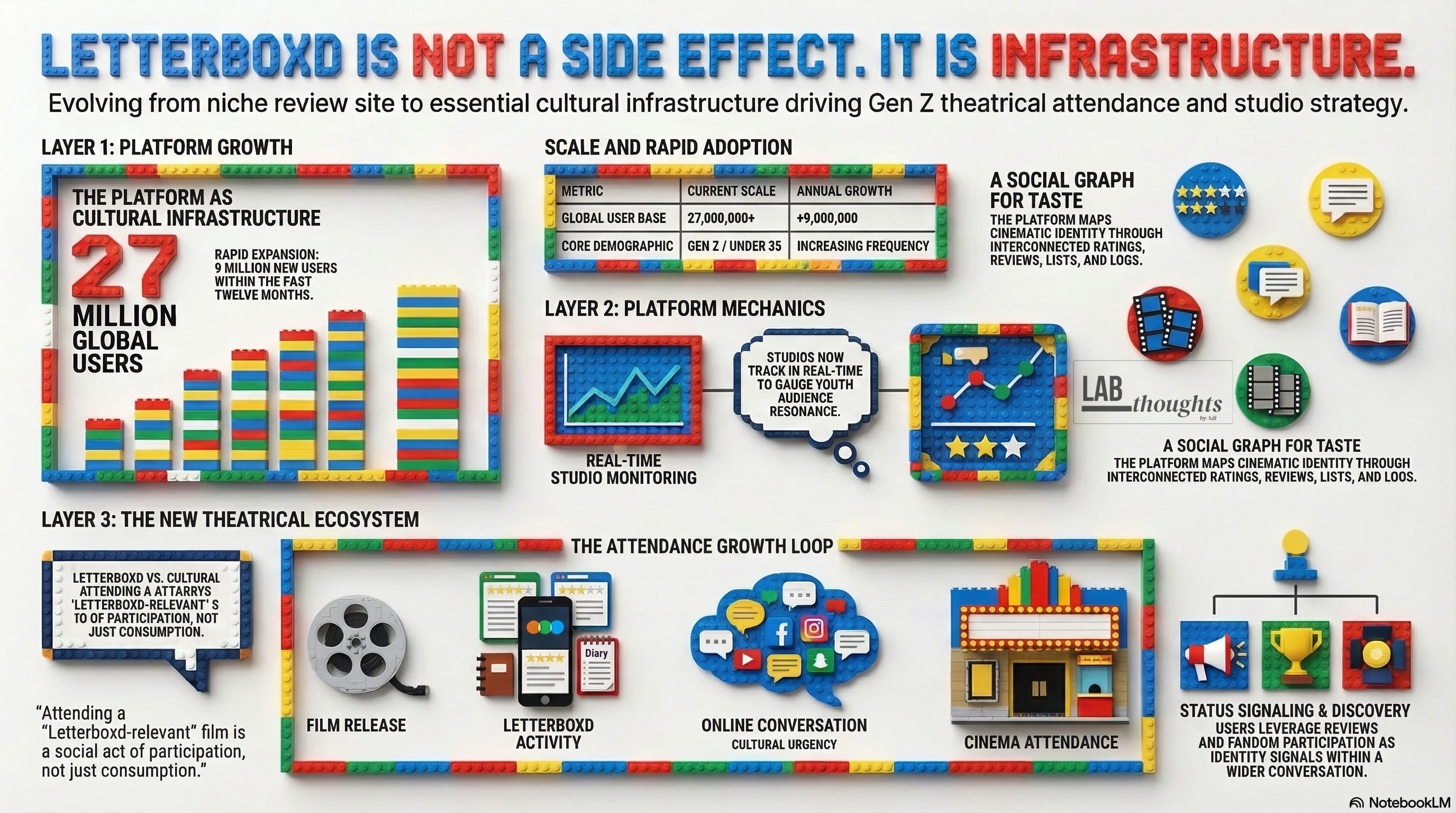

Letterboxd, which grew by 9 million users in the past year to more than 27 million globally is not incidental to this shift. It is infrastructure.

Studios are now watching Letterboxd ratings in real time to gauge how films are resonating with younger audiences. The platform functions as a social graph for cinematic taste, and Gen Z knows it. Attending a film that matters on Letterboxd is participating in a conversation, not just consuming content.

Ray Subers, head of film at NRG, framed it cleanly: Gen Z goes more frequently than older audiences and gravitates toward IP from video games, anime, and YouTuber brands, as well as animated films they grew up on. His words: “Gen Zers don’t want their parents’ franchises.”

That sentence is worth sitting with. It is not an anti-franchise sentiment. Gen Z turned out in force for Zootopia 2 and Scream 7. What it means is that the franchise has to belong to them, not to the 45-plus demographic that studios have been optimising for since the mid-2000s.

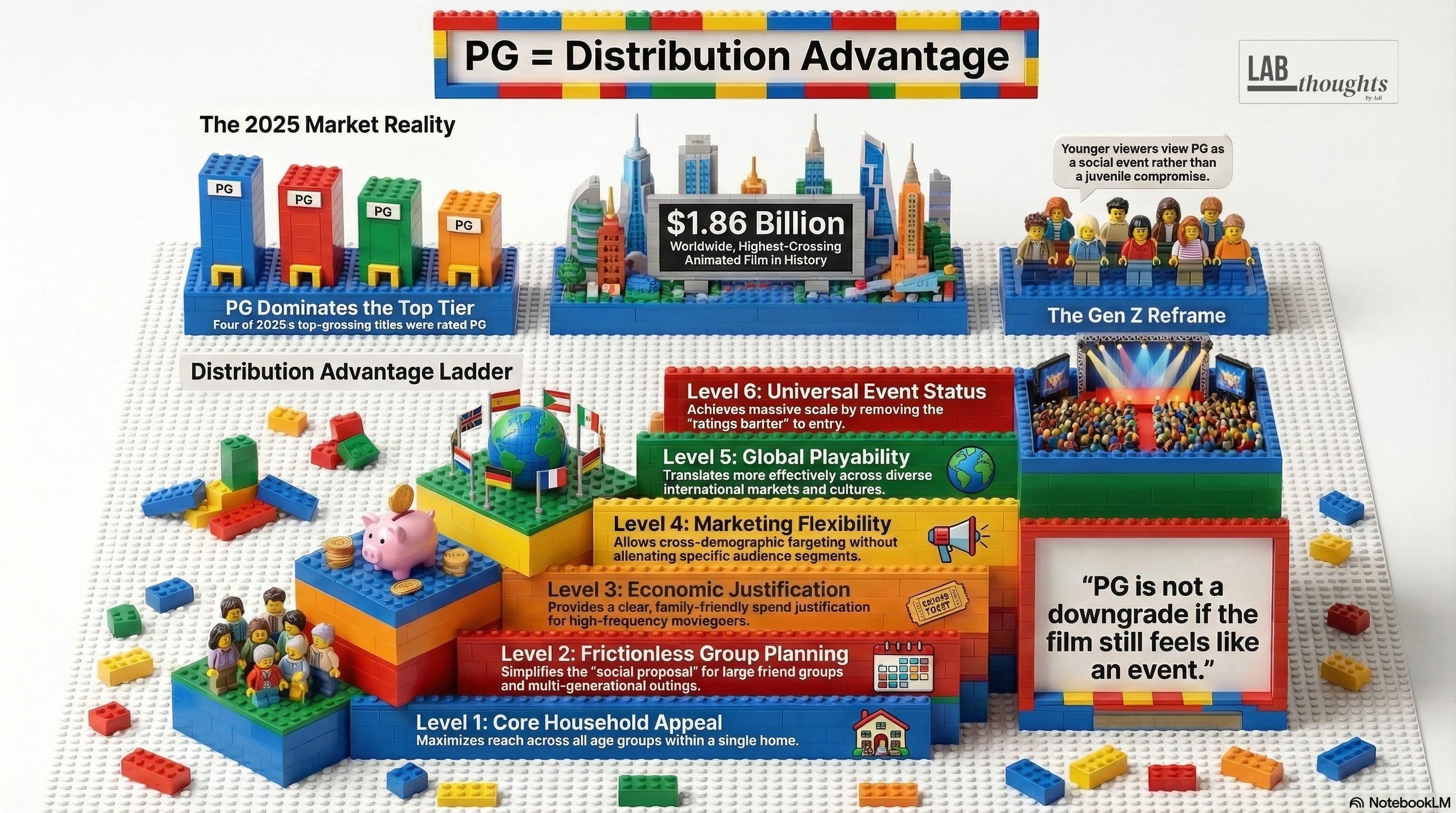

PG is back, and that is not a small detail

For a decade, PG was treated as compromised inventory. Too soft for teenagers, too juvenile for general audiences. The conventional wisdom, earned partly from millennial behaviour, was that teens in particular rejected all-ages branding as uncool.

Gen Z appears less allergic to it. Four of 2025’s top titles were PG. That changes the economics in several useful ways.

A PG film travels further in households, easier to coordinate as a group, easier to justify as a family spend, easier to market across demographics without alienating any of them. And PG does not mean safe or small. Zootopia 2 is not a modest film. It is the highest-grossing animated film in history.

The reframe is this: PG is not a downgrade if the film still feels like an event. It is a distribution advantage.

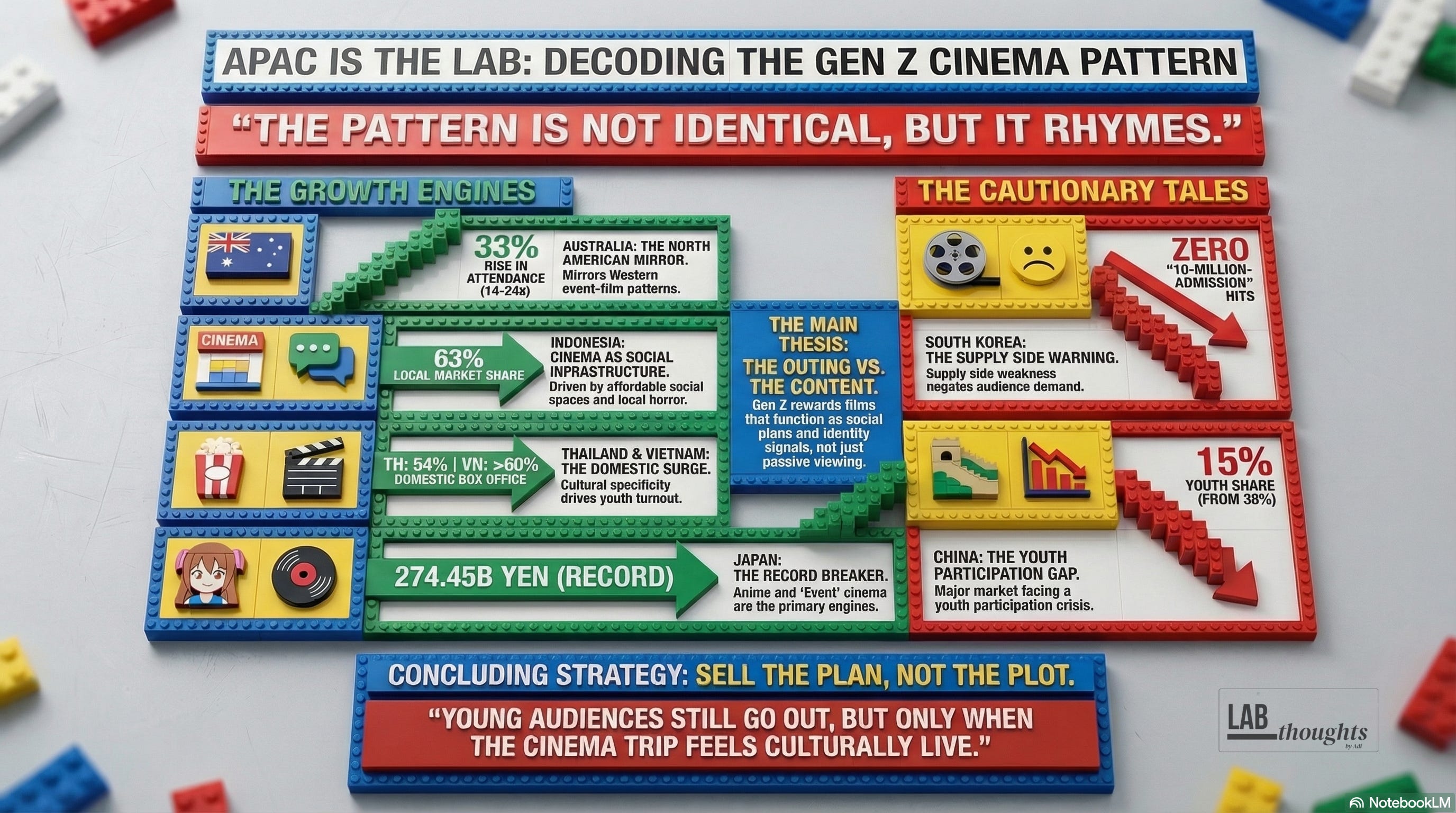

APAC is the lab

Here is where the story gets more interesting, and more useful, than the North American read alone.

Australia mirrors the North American pattern closely. Screen Australia’s data through 2024 shows 14-24-year-olds are the most likely age group to attend cinema and the most frequent attendees, over-indexed against their population share.

Over the Australian 2025-26 summer season, admissions rose strongly, with the P14-24 cohort up 33% and P18-39 up 20%, alongside a significant family-film boost. Family animation, horror, social-native titles, and broad-audience event films are doing the heavy lifting. Familiar picture.

Indonesia tells a more structural story. Local animated film Jumbo passed 9.6 million viewers and took over $20 million at the box office, becoming Indonesia’s highest-grossing animated film (Reuters, 2025).

Cinema 21 recorded its highest-ever April moviegoer count. Local films held 63% market share year-to-date in 2025. Horror has been the mainstay of Indonesia’s post-pandemic theatrical business, with Pabrik Gula becoming the country’s top-grossing film at that point in 2025.

What Indonesia shows is that when cinema functions as affordable social infrastructure, and the supply side is culturally specific, young audiences are a genuine theatrical tailwind, not just a supporting statistic.

Thailand and Vietnam are producing similar signals. Thai films reached 54% of the domestic box office in 2024, ahead of Hollywood at 38% (Screen Daily). How to Make Millions Before Grandma Dies became a regional phenomenon. Vietnam saw domestic films account for more than 60% market share in 2025. '

Japan had a record box office year at 274.45 billion yen in 2025, driven substantially by local anime and event cinema.

The pattern across these markets is not identical, but it rhymes. Young audiences still go out. They go out for animation, horror, local-language hits with cultural specificity, premium-format spectacle, and films that have social conversation value before and after the screening. The cinema trip has to feel culturally live, not like catching up on content you missed.

South Korea is the cautionary data point. 2025 was the first non-pandemic year since 2012 with no Korean film crossing 10 million admissions, and total admissions fell sharply year-on-year (KOFIC).

Young audiences in Korea have not stopped caring about cinema culture. The supply side weakened, investment contracted, and fewer breakout titles made it through. Audience willingness is necessary but not sufficient. You still have to give them something worth seeing.

China complicates the simple “Gen Z is back” story further. Variety reported that audiences under 24 represented only 15% of Chinese moviegoers in 2025, down from 38% pre-pandemic. That is a massive market with a youth theatrical problem that has no easy fix.

The APAC read, across all of this, is the same sentence in multiple dialects: young audiences still go out, but only when the cinema trip feels like something worth leaving the house for.

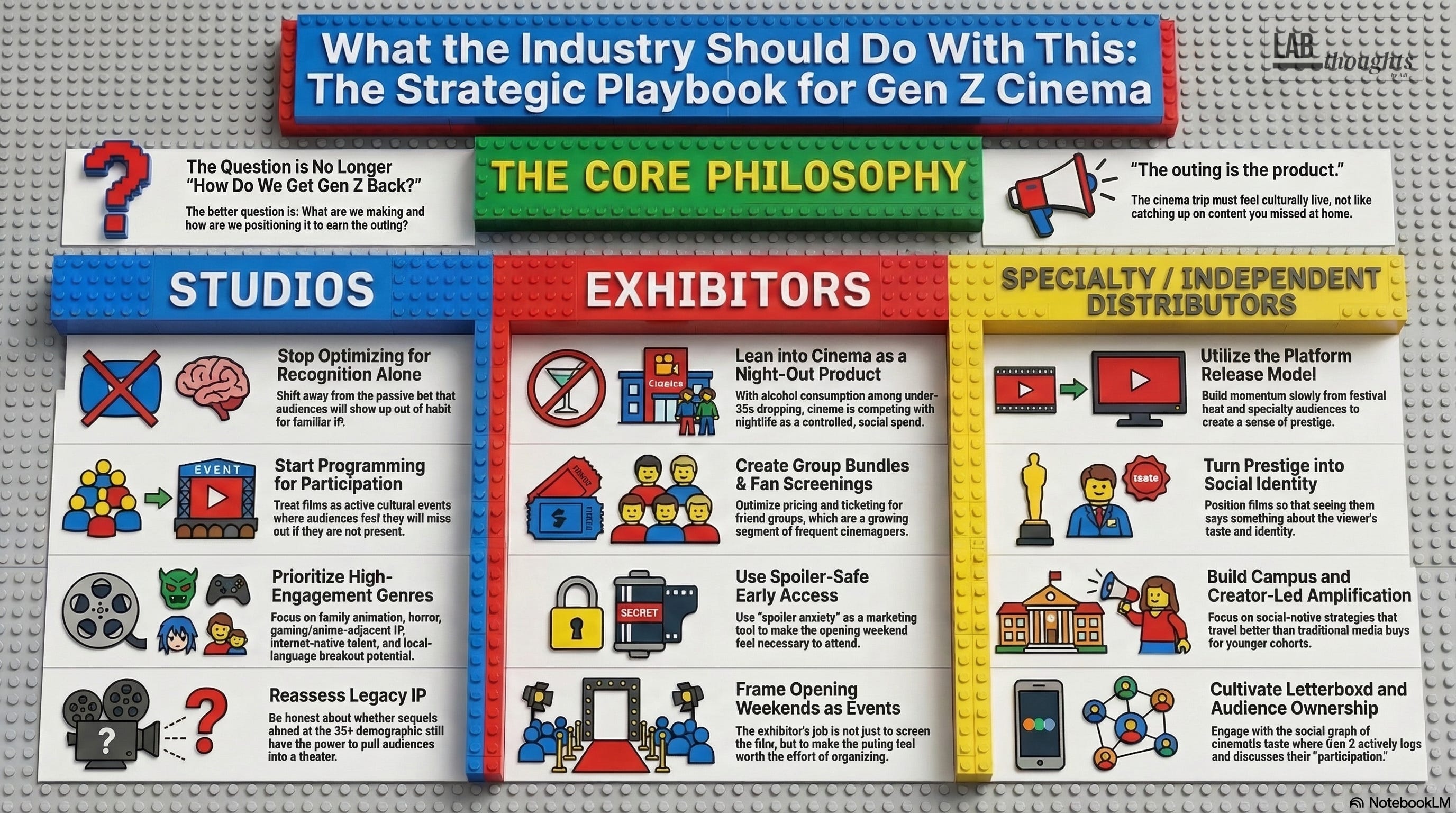

What studios, exhibitors, and indie distributors should do with this

The strategic question is not “how do we get Gen Z back?” They are back, selectively and on their terms. The question is what you are making and how you are positioning it to earn the outing.

For studios

Stop optimising for recognition and start programming for participation. Recognition says: this IP is familiar, the audience will show up out of habit. Participation says: this film is a cultural event, you will miss out if you are not there. The first is a passive bet. The second is an active one.

Prioritise by what travels in groups and generates conversation: family animation, horror, gaming and anime-adjacent IP, internet-native talent projects, local-language breakout potential, and anything with a clear social hook.

Legacy IP aimed primarily at the 35-plus demographic is a shrinking return in theatrical.

That does not mean abandon sequels. It means ask honestly who the sequel is for and whether that audience still goes out.

For exhibitors

The cinema trip is competing with nightlife and winning partly on economics. Gallup found the share of US adults under 35 who say they drink fell from 72% in 2001-2003 to 62% in 2021-2023. Gen Z is economically literate and socially motivated. A cinema trip is a controlled spend with a predictable social outcome. Lean into that.

Group bundles, fan screenings, spoiler-safe early access, and event framing around opening weekends are not gimmicks. They are product design.

The exhibitor’s job is not just to screen the film. It is to make the outing feel worth organising.

For specialty and independent distributors

The good news from the THR piece is that specialty market share is recovering. Neon, A24, Focus Features, and Searchlight held 7% of domestic box office in 2025, up from 4% the year before.

Gen Z is turning out for Oscar nominees and prestige titles when they arrive as events rather than homework.

The platform release model, building slowly from festival heat and specialty audiences outward, is working again. Prestige plus social identity is a viable positioning: the film that says something about you for having seen it.

Campus and creator-led amplification, Letterboxd community cultivation, and audience ownership at the platform level all travel better than traditional media buys for this cohort.

The new theatrical playbook

The through line across all three audience types is this:

Sell the plan, not just the plot. A film is not a product description. It is a social proposal. The marketing job is to make the outing feel easy to coordinate and necessary to attend.

Program for groups. Single adult without children is now a larger share of frequent cinemagoers than pre-pandemic [FYI - This here is me reading between the lines, based on directional industry data through 2025].

Friend groups, not just couples and families, are a growth segment. Build ticketing, pricing, and in-cinema experience around them.

Design for reaction, not just reach. The trailer gets them aware. The fancam, the Letterboxd review, the spoiler anxiety, and the group chat argument are what close the sale.

Distribution strategy that does not account for the social aftermath of a film is only half a strategy.

Treat spoilers as a marketing pressure valve. The fear of missing out is real and commercially useful. Films that generate genuine spoiler anxiety before opening weekend are telling you that you have a live cultural event. That is worth protecting and amplifying.

Build films people can wear, quote, log, argue about, and recommend to a stranger online.

Not every film can do all of these. But every studio greenlight decision should ask how many of these the project makes possible.

The question Hollywood keeps asking wrong

Can Gen Z save Hollywood?

They can stabilise theatrical momentum. They can rescue specific genres faster than others. They can force studios to confront stale assumptions about what younger audiences want.

They cannot save an industry that keeps overspending on dead IP, underestimating its audience’s cultural literacy, and scheduling expensive films for people who would genuinely rather stay home.

Gen Z will buy the ticket. They will not perform CPR on a franchise out of courtesy. The films that earn the outing, earn it clearly. The ones that do not, will find out the hard way that recognition is not demand, and awareness is not anticipation.

The markets paying attention to this, from Sydney to Jakarta to Tokyo, already know what theatrical is still good at.

The question is whether the boardrooms in Los Angeles are watching closely enough.

So tell me what was the last film you saw in a cinema because missing it felt like missing something, not just something you wanted to watch?

If this raised a question about a project you are working on, email me at adi.tiwary08@gmail.com. I work with producers, development teams, and strategists on projects that need sharper positioning, stronger buyer legibility, or clearer rights strategy. The best place to start is a Project Audit.