Every format boom eventually stops talking about creativity and starts talking about infrastructure.

That is usually the moment when you know it is real.

Ahead of FilMart next week, COL Group and BeLive unveiled what they call “Microdrama in a Box”: a white-label app stack that bundles catalogue, infrastructure, monetisation tools, AI subtitling, and gamification into something a buyer can launch in 30 days. The phrase is clunky. The strategy is not.

Because this is not really about microdrama content at all. It is about owning the rails before everyone else in Southeast Asia, MENA, and Latin America realises the format has moved from trend to infrastructure.

What they are actually selling

The Deadline headline calls it “Microdrama in a Box.” That framing is more accurate than it sounds.

COL Group brings the IP pipeline: it is one of the largest producers of vertical short-form drama globally, with international distribution deals announced at MIP London last week.

BeLive Holdings, via its Yeon Studios arm, brings the platform plumbing: a vertical episodic playback engine, built-in gamification and reward mechanics, ad and subscription monetisation frameworks, multi-language AI subtitling, and optional commerce integration.

Together, they are not pitching a content deal. They are pitching a business model, flat-packed and ready to ship in 30 days.

That is a meaningful distinction. Most content licensing deals require the buyer to build the product layer themselves, work out the retention mechanics, and figure out monetisation through trial and error. This offer skips all of that. The buyer focuses on brand positioning and go-to-market. COL and BeLive handle everything behind it.

Timothy Oh, General Manager of COL Group International, put it plainly at FilMart: “We’re removing operational complexity for our partners.” (Deadline, March 4, 2026.)

Why Southeast Asia is the real target

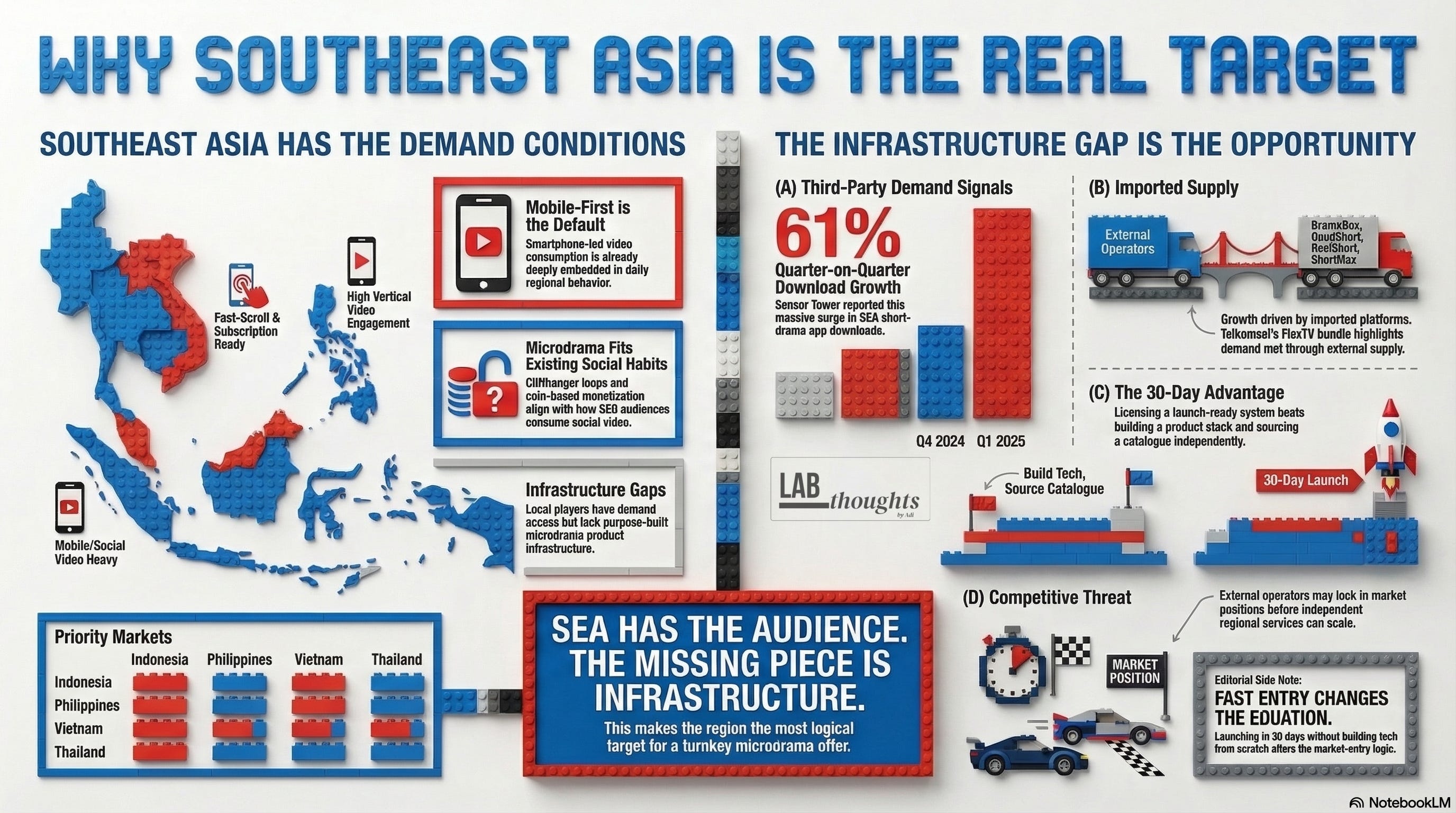

COL and BeLive name Southeast Asia, MENA, and Latin America as the addressable markets. That is a broad sweep. But Southeast Asia is where this offer lands with the most force, and it is worth being specific about why.

SEA has the demand conditions without the infrastructure. Mobile-first consumption is not a trend here. It is the default. In markets like Indonesia, the Philippines, Vietnam, and Thailand, smartphone penetration and mobile data affordability have outrun platform investment for years. Local OTT players, telcos with entertainment bundles, and regional broadcasters have audiences ready for this format. What they lack is the product stack to serve it properly.

Microdrama’s behavioural mechanics, short episodes, cliffhanger-driven loops, and coin-based or subscription monetisation, map well to how SEA audiences already consume social video. ReelShort and DramaBox have both reported strong engagement numbers from SEA audiences engaging with Chinese-originated content.

That regional appetite is visible in third-party market data: Sensor Tower reported Southeast Asia short-drama app downloads rose 61% quarter on quarter in Q1 2025, while Omdia identified DramaBox, GoodShort, ReelShort, and ShortMax among the apps driving Asia’s growth.

In parallel, operator deals such as Telkomsel’s FlexTV bundle in Indonesia suggest that a meaningful share of current demand is being served by imported platforms and catalogues rather than a mature field of local standalone services.

The COL and BeLive offer is explicitly aimed at filling that gap before local competitors do. If a telco in Indonesia or a broadcaster in the Philippines can launch a branded microdrama app in 30 days without building the tech or acquiring a catalogue from scratch, the cost-benefit calculus changes sharply. (a phrase that still gives me mild school-related flashbacks).

That is the real competitive threat this product poses to anyone thinking about entering this space independently.

The infrastructure phase is now

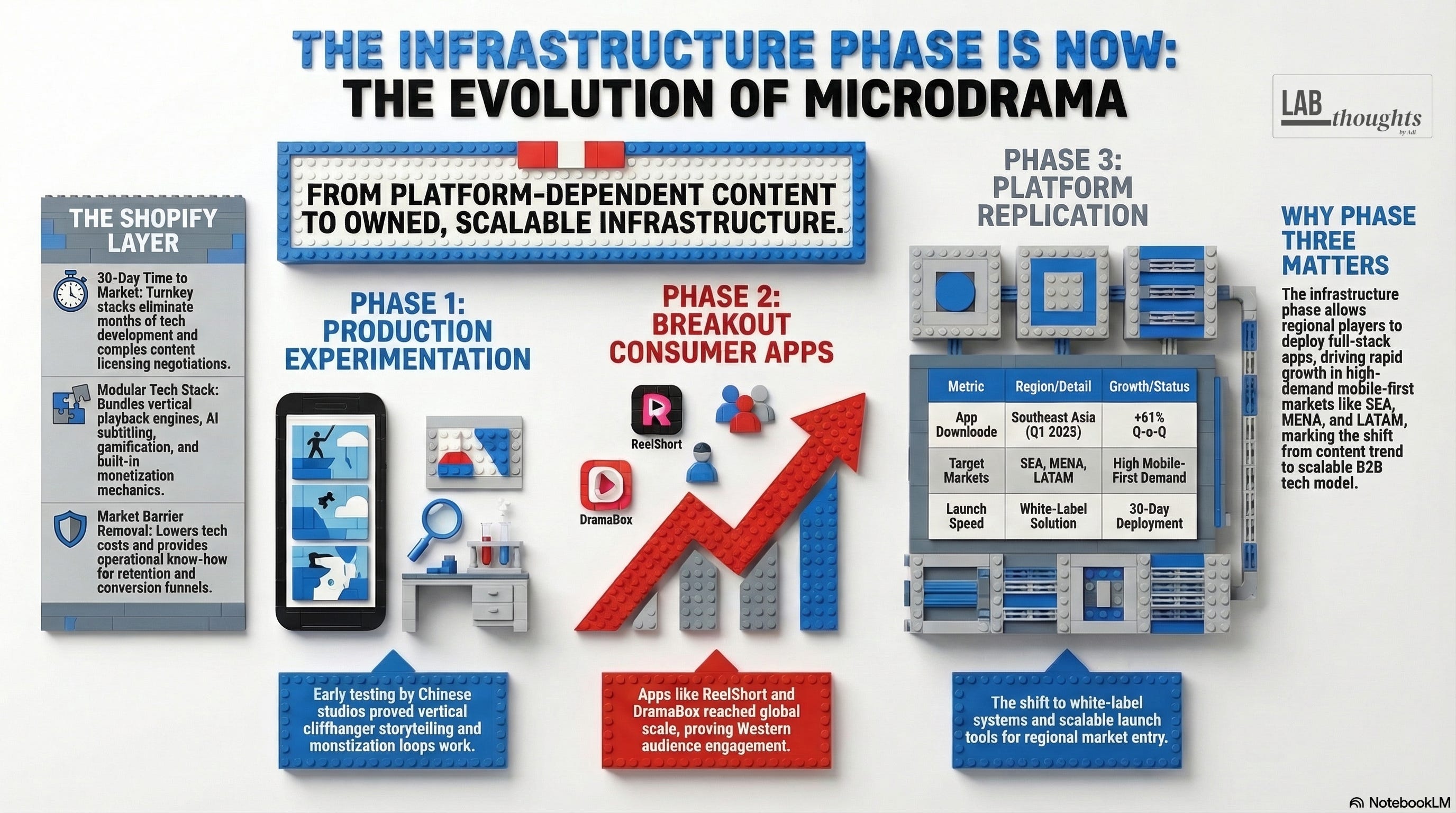

Microdrama has moved through two phases quickly.

Phase one was production experimentation: Chinese studios and independent developers testing the format and finding that the economics worked if you got the cliffhanger mechanics and monetisation loops right.

Phase two was breakout consumer apps: ReelShort, DramaBox, ShortMax, and others reaching scale in the US and globally, demonstrating that Western audiences would engage with the format.

Phase three, the one COL and BeLive are now naming, is platform replication. The B2B infrastructure play. The Shopify layer. Once this phase takes hold, microdrama stops behaving like a content trend and starts behaving like a content-tech franchise model. That is when the distribution economics change permanently.

Latif Sim, Executive Director of BeLive Holdings, framed this in the announcement as turning “microdrama from platform-dependent content into owned, scalable infrastructure.” (Deadline, March 4, 2026.)

That is not marketing language. It is an accurate description of what the product is trying to do.

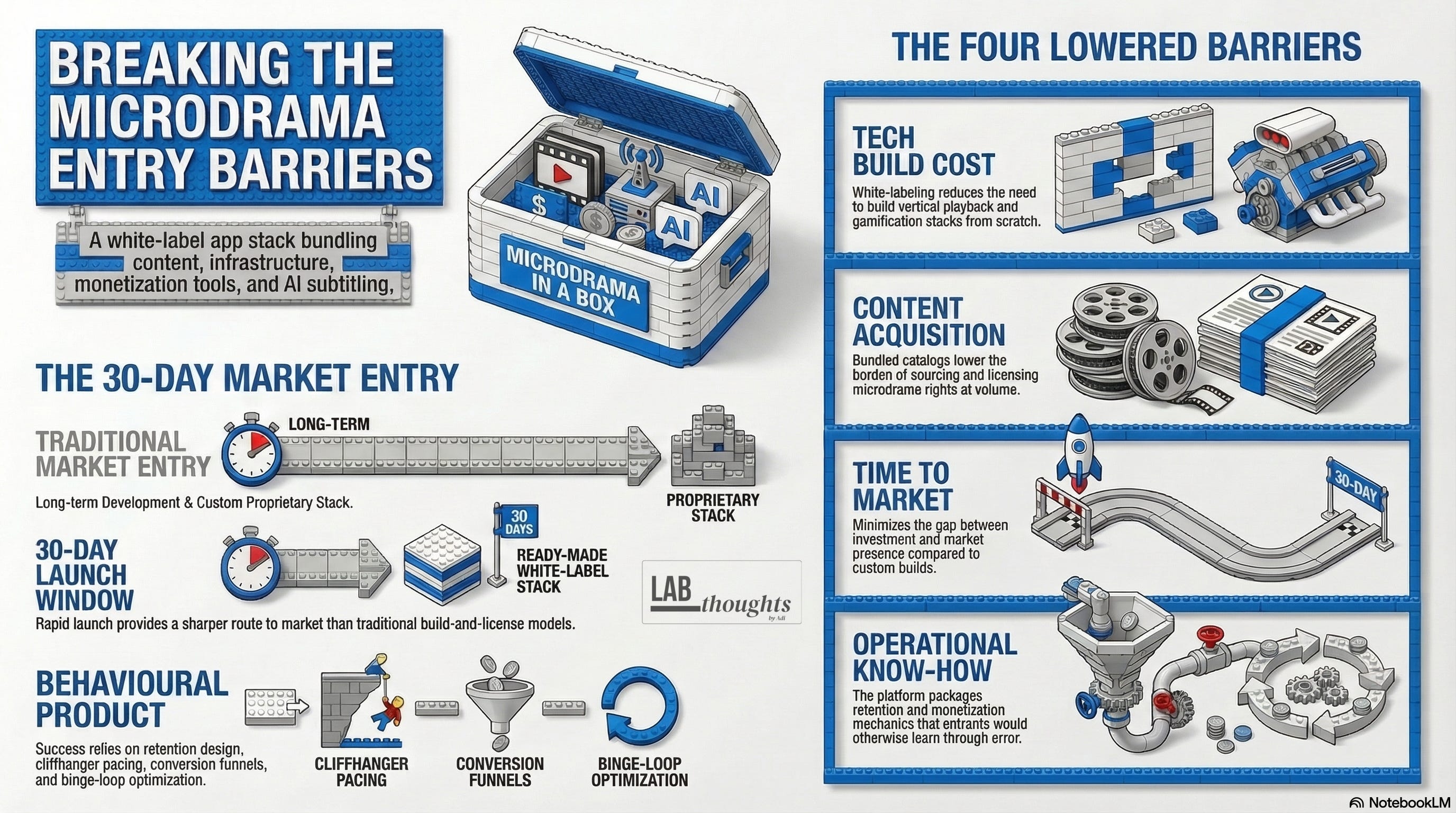

The four barriers it actually lowers

The pitch works because it addresses the four real blockers for any new market entrant:

Tech build cost. A vertical episodic playback engine with gamification and monetisation tools is not cheap to build or maintain. White-labelling eliminates that capital requirement.

Content acquisition complexity. Licensing microdrama content at volume, and at the quality consistency needed to drive retention, requires relationships and deal-flow that most regional players do not have.

Time to market. Thirty days to launch is not a feature. It is a market-capture strategy. In a format moving this fast, 30 days versus 18 months is a genuine competitive advantage.

Operational know-how. This is the sleeper issue. Plenty of buyers can license content. Far fewer know how to optimise a vertical episodic app for retention, cliffhanger pacing, ad load, conversion funnels, and binge loops.

Microdrama is not short TV. It is a behavioural product. The operational knowledge embedded in BeLive’s platform is not trivial.

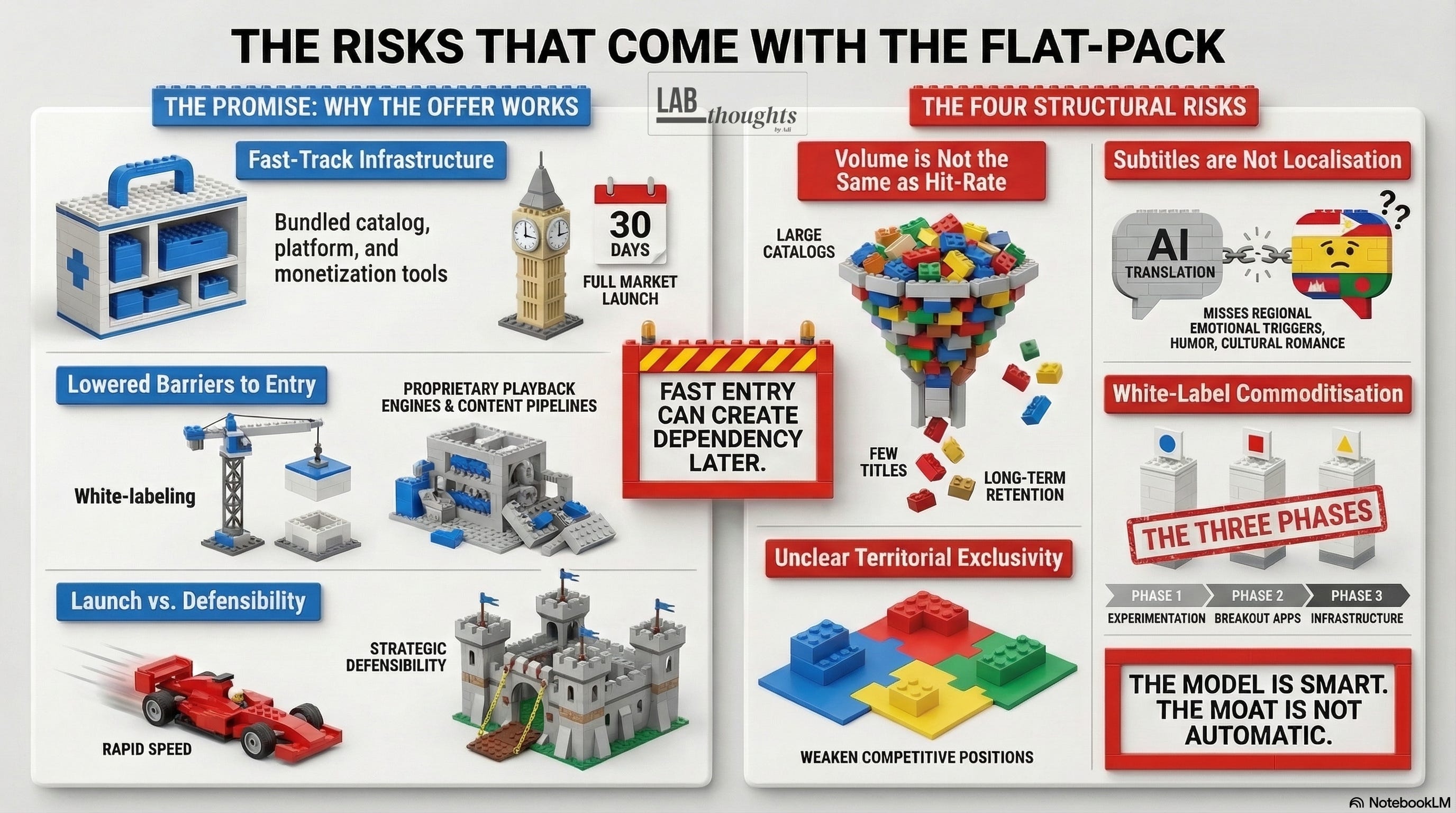

The risks that come with the flat-pack

The offer is smart. It is not bulletproof.

Catalogue fatigue is the first problem. Even a very large catalogue is not the same thing as consistent hit-rate quality. As the market matures and audiences become more selective, sheer volume becomes less of an advantage. What matters is the proportion of titles that can actually anchor a retention loop.

Cultural localisation runs deeper than subtitles. COL’s AI subtitling handles language. It does not handle the emotional triggers, romance codes, humour registers, and pacing preferences that vary significantly between Indonesia, the Philippines, Vietnam, and Thailand, let alone between SEA and MENA. A platform that feels like translated Chinese product rather than locally resonant content will face a ceiling on long-term retention.

White-label commoditisation is the structural trap. If multiple telcos and OTT players in overlapping territories launch near-identical apps with the same content catalogue, differentiation disappears. The buyer’s brand sits on top. The product underneath is the same.

Now that is fine as a launch strategy, but it becomes a problem when audiences and advertisers start to notice.

Territorial exclusivity is the question serious buyers will be asking as FilMart opens. If a telco in Indonesia and a broadcaster in the Philippines can both launch with the same catalogue, what is the competitive position of either?

The answer to that question will determine whether this offer has long-term strategic value or is a fast-launch shortcut that creates a dependency problem later.

What to watch

The announcement is the easy part. The signal is in what happens next.

Watch which territories sign first and what category of buyer commits. Telcos and broadcasters indicate different things about where the demand is actually sitting.

Watch whether COL offers market-specific catalogue exclusivity or whether the model is volume-first. That distinction matters more than the 30-day launch window.

Watch whether commerce integration, the optional layer in the current offer, gets taken up seriously.

In SEA markets where social commerce is already embedded in daily consumption behaviour, commerce integration is not an optional feature. It is the most defensible monetisation layer available.

Watch the ARPU data once platforms launch. Gamification and reward mechanics can drive engagement. Whether they drive sustainable monetisation in markets with lower consumer spending power than the US is a different question.

A closing thought from the lab

The real test is whether anyone here is building a business, or just renting one

COL and BeLive have correctly read that the next competitive advantage in microdrama is not making more content. It is owning the rails other people’s content runs on.

The timing is shrewd. FilMart is exactly the kind of market context in which this pitch makes sense, because the buyers are there and the infrastructure gap in Southeast Asia, MENA, and Latin America is real enough to make a fast-launch offer attractive.

The question is not whether this product finds customers. It will. The question is whether it creates sustainable competitive positions for those customers, or whether it produces a generation of commodity microdrama apps that look identical, chase the same audiences, and wonder in 18 months why retention is plateauing.

Shopify made a lot of merchants. Not all of them built defensible businesses.

That is the real test.

And it is probably the right question to leave hanging over this model: are buyers here building something defensible, or just getting to market faster on rented infrastructure?

Sources: Deadline (Jesse Whittock, March 4, 2026); COL Group and BeLive Holdings statements at FilMart, March 2026.

If this raised a question about a project you are working on, email me at adi.tiwary08@gmail.com. I work with producers, development teams, and strategists on projects that need sharper positioning, stronger buyer legibility, or clearer rights strategy. The best place to start is a Project Audit.