TL;DR: India’s creator economy is the largest and fastest-growing in APAC. It is also the most structurally broken. Only 8-10% of creators generate sustainable revenue, compared to roughly 40% in mature Western markets. The problem is not a lack of talent or audience. It is a packaging and distribution problem. The next wave of winners will not be amateur entertainers optimising for algorithmic virality.

A few weeks ago, a member from the Lab Thoughts community, an Indian format creator with twenty years building unscripted IP across APAC, put a question to me I could not shake: "Is there an experimental playbook for Tier 2 and Tier 3 cities we can run?"

I did not have one ready. But the conversation exposed a gap. It made the market feel less like an abstract “creator boom” headline and more like a system hardening in real time. And it hit home, because my own roots are in Tier 2 India. I know what scale looks like when it is not metro-first.

If something sticks in my head, we take it to the Lab.

Short answer: the playbook is no longer experimental. The results are in. What is missing is not the evidence. It is operators willing to run the system.

But the Tier 2/3 question turned out to be the last question, not the first. Before you can run a vernacular playbook, you need to understand what kind of IP you are running it with.

Lets being with the shift

A cardiologist in Pune films a Reel between consultations. A corporate lawyer in Hyderabad records a YouTube explainer on her lunch break. A UX designer in Bangalore packages a Figma template and drops it into a TagMango storefront.

They have more domain authority than most of the creators who are actually making money in India right now. And that gap, between expertise and monetisation, is the most expensive unsolved problem in APAC digital media.

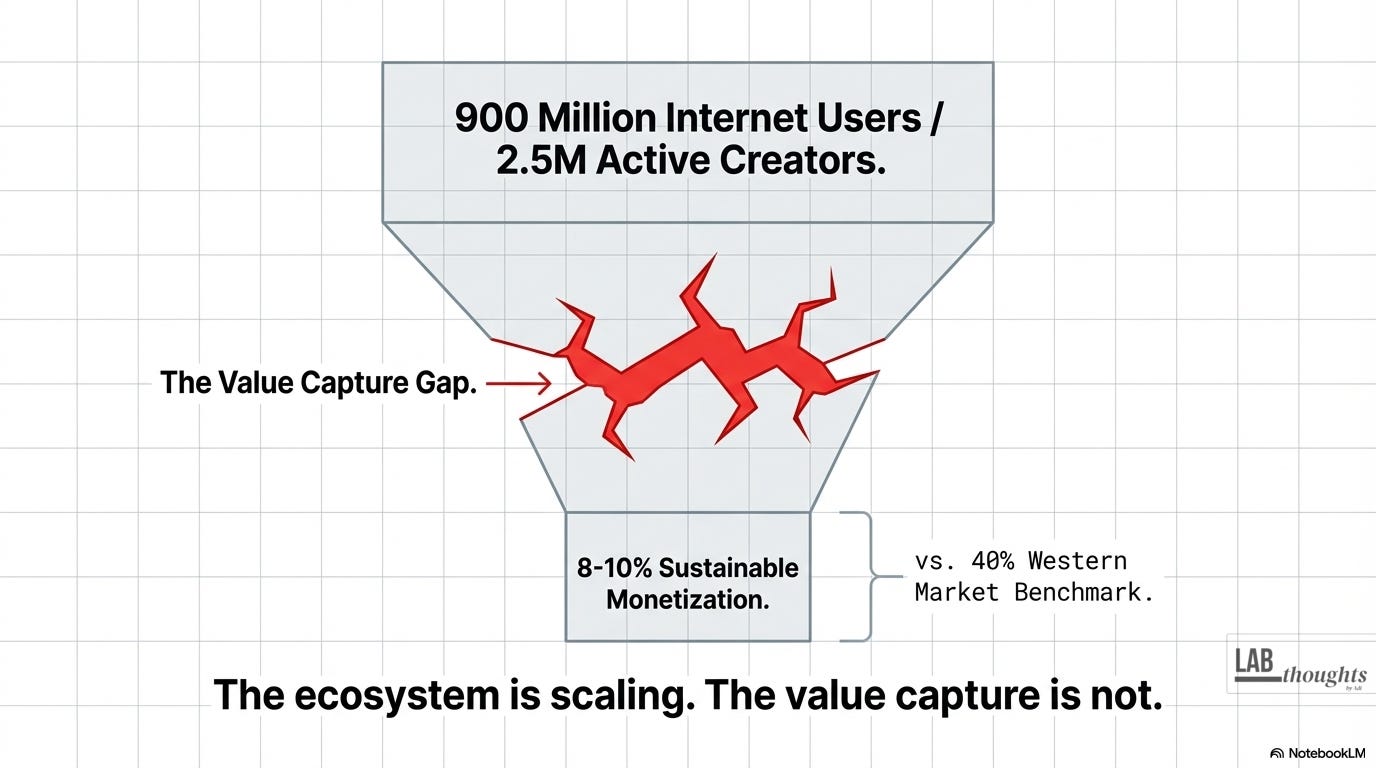

The numbers frame the scale. India currently has over 900 million internet users. The creator economy was valued at approximately USD 12.28 billion in 2025 and is projected to reach USD 49.83 billion by 2032 at a compound annual growth rate of 22.2% (Coherent Market Insights, 2025).

Digital media has become the largest segment of the Indian media and entertainment sector, contributing about 32% of revenues in 2024. Digital advertising reached approximately INR 700 billion in the same year, taking a roughly 45-46% share of total Indian ad spend (EY/FICCI-EY report, 2024; CRISIL, 2025).

Now those are not social media metrics. Those are industrial economics.

But here is the structural fracture underneath the growth story.

Out of approximately 2 to 2.5 million active digital creators in India (defined as those with 1,000-plus followers), only 8-10% monetise effectively (BCG/Government of India, 2024).

In mature Western markets, the equivalent figure sits around 40%. Some 42,000 Indians now earn their primary income as creators, a 250% increase from prior years, but 88% of active creators still depend on day jobs, freelance income, or family support (Exif Media, 2025).

The headline growth obscures a winner-takes-most reality. Influence is concentrated at the top. Less than 5% of channels account for 90% of subscriptions on dominant video platforms (Kotak MF, 2025).

Now the ecosystem is scaling.. but the value capture is not.

That monetisation gap is the story. Not who is creating. Who is capturing.

The gap: craft versus product

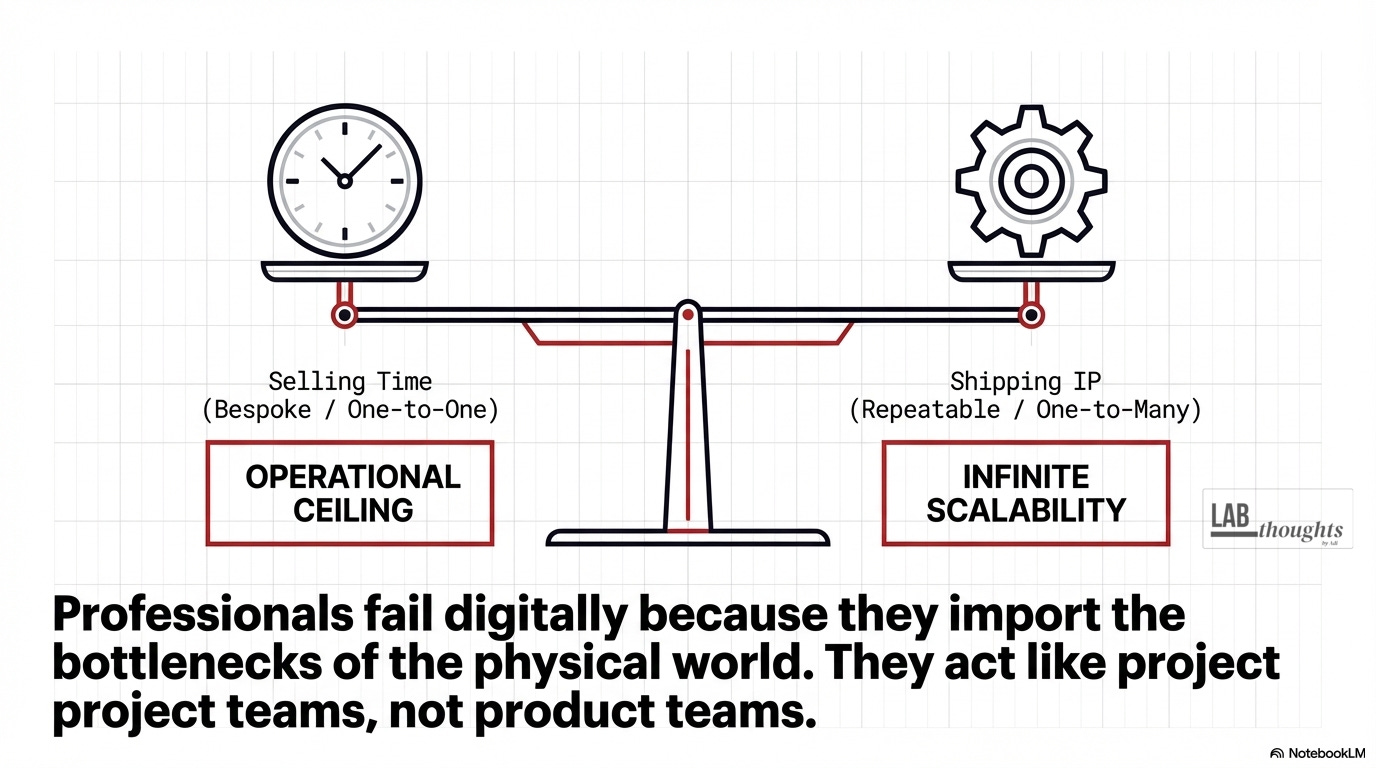

The fundamental reason established professionals struggle in the creator economy is not a content problem. It is an operating model problem. And the framing that clarifies it comes from product thinking, not media theory.

Professionals are trained to deliver bespoke craft. A doctor evaluates one patient at a time. A lawyer drafts a contract tailored to one entity’s liabilities. A designer conceptualises a UI for one client’s brand architecture. The compensation model rewards time, diagnostic skill, and customised execution.

When these professionals pivot to digital, their first instinct is to replicate the offline model online. Synchronous consulting hours. Individualised coaching. Highly specific freelance services via social platforms. They import the bottlenecks of the physical world into the digital realm and immediately hit operational ceilings.

Silicon Valley Product Group frames the distinction cleanly: product teams are durable and outcome-oriented; project teams exist to deliver a release and move on.

Creators who win over time behave like product teams. They own a loop, content to distribution to monetisation to reinvestment, and iterate.

Professionals who lose behave like project teams. They deliver an output and start again from zero.

The failure to transition from a one-to-one service provider to a one-to-many digital architect is the primary reason the professional creator gap exists.

And the secondary reason is equally structural: most professionals lack the cognitive framework for digital productisation. They assume clinical or technical superiority will automatically guarantee market success. It does not.

A study of Indian medical startups found founders repeatedly failed because they focused entirely on clinical efficacy while neglecting go-to-market strategy, user experience packaging, and the relational trust required to drive mass adoption.

I think the same pattern applies across legal, financial, and design verticals. The “curse of knowledge” renders deeply valuable information invisible in a social feed optimised for immediate visual and emotional resonance.

This is the craft-versus-product split. And it is the same split Lab Thoughts has explored in the Brand as Studio series: the difference between making something good and making something that survives a market.

The IP architecture: identity, format, operating rhythm

In the creator economy context, “intellectual property” is not a legal filing. It is an operational framework. True creator IP is the proprietary combination of three components: identity, format, and operating rhythm.

Together, they transform commoditised professional knowledge into a defensible, monetisable digital asset.

Identity is the trust layer.

In the digital economy, institutional prestige, the degree from a premier university, the title at a prestigious firm, holds diminishing returns on platforms driven by parasocial relationships. Trust is not granted by institutional authority. It is engineered through authenticity, consistency, and empathetic communication.

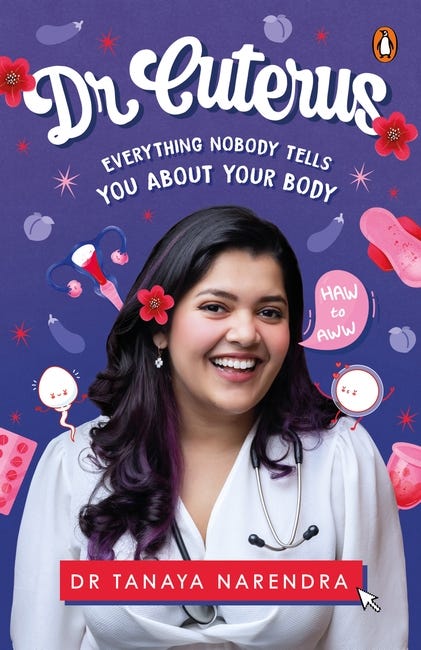

The case study that illustrates this most precisely in India is Dr. Tanaya Narendra, known digitally as “Dr. Cuterus.” She combined rigorous academic credentials (MBBS, MSc from Oxford) with a highly accessible, humour-driven persona to normalise historically taboo conversations about reproductive health.

Her identity itself became the core IP. It allowed her to package knowledge into a bestselling book, scale through vernacular translations, secure brand partnerships, and assume advisory roles with government bodies including NITI Aayog.

The persona is not a marketing layer. It is the product.

Format is the repeatable container.

Once an identity is established, the professional must translate expertise into scalable formats. This is the transition from craft to product. Knowledge must be fractured, organised, and repackaged into discrete, consumable units that solve specific, high-urgency problems for a targeted niche.

In India, the dominant format categories are: high-ticket cohort-based courses and intensive workshops (commanding premium pricing by promising specific, measurable transformations rather than information transfer); tiered membership communities (transforming passive audiences into predictable recurring revenue); and digital-physical hybrid products (bundling digital educational content with tangible physical tools to alter perceived value and build deeper trust).

The legal education platform LawSikho exemplifies format mastery at enterprise scale: it identified a systemic skills gap between Indian law school curricula and working law firm demands, formatted legal expertise into application-oriented digital courses, and built an enterprise robust enough to execute an SME IPO. That is shipping a product, not a craft.

The operating rhythm keeps the work moving.

Professionals fail when they treat content creation as an ad-hoc, inspiration-driven activity. Successful IP packaging requires a rigorous operational rhythm: top-of-funnel short-form content captures attention, mid-funnel long-form content (podcasts, newsletters, webinars) builds trust, and a conversion event captures value.

The rhythm prevents burnout by shifting focus from constant ideation to execution of a defined, automated funnel.

For anyone who has worked in format development for television, this three-part architecture should sound familiar.

Identity is the “show bible” talent attachment.

Format is the repeatable episode structure.

Operating rhythm is the broadcast schedule.

The creator economy is not inventing new mechanics. It is applying format logic to a different distribution surface.

The distribution loop: escaping the algorithmic treadmill

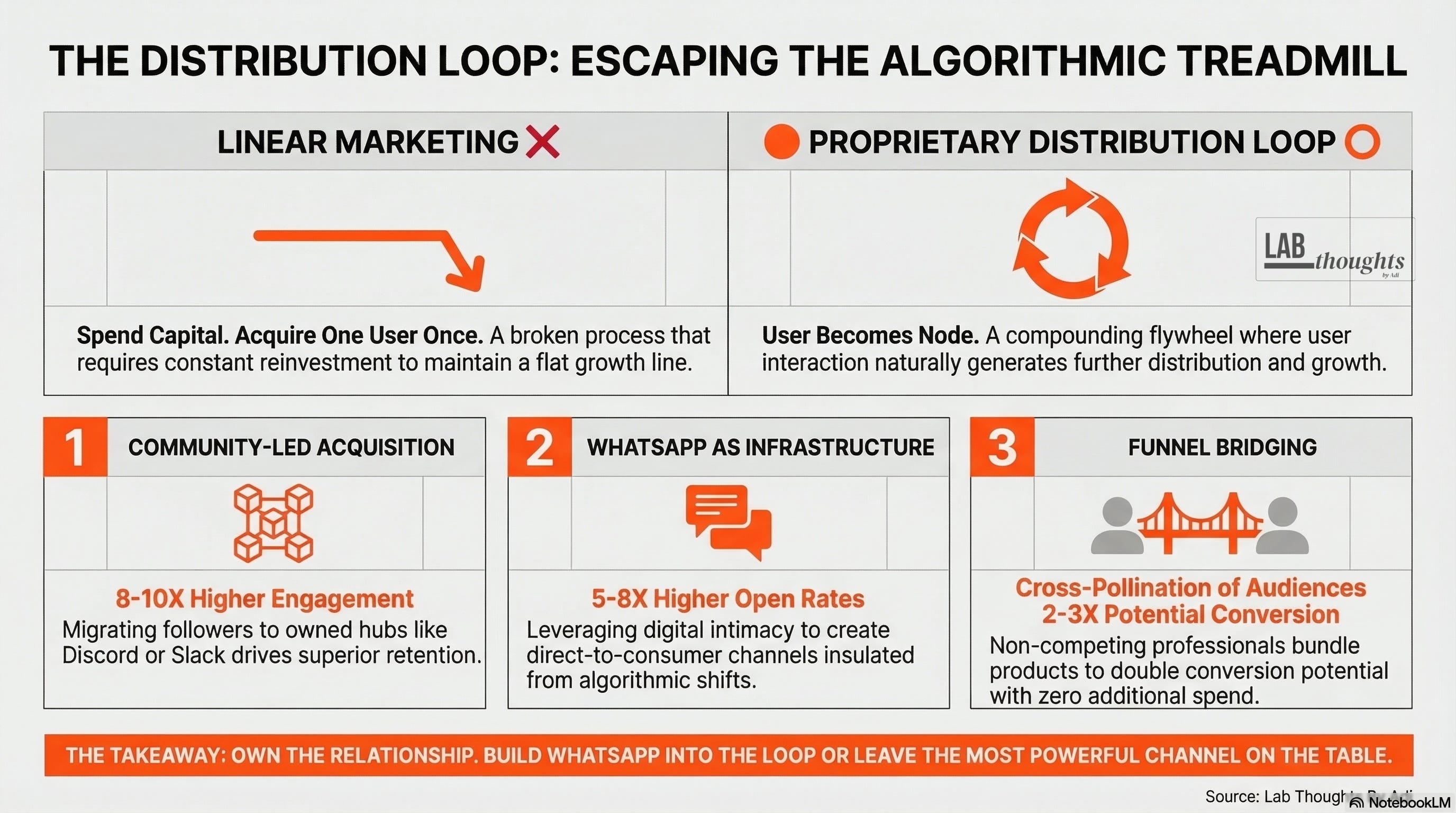

Creating robust, formatted IP is half the equation. The other half is distribution. And the defining characteristic of the most successful knowledge creators in India is in their ability to construct proprietary distribution loops.

A distribution loop is a self-sustaining cycle in which a user’s interaction with content naturally generates further distribution, acquiring new users without proportional increases in marketing spend.

It is a compounding flywheel effect that reduces customer acquisition cost over time. Linear marketing spends capital to acquire one user once. A distribution loop turns each user into a distribution node.

In India, three loop mechanics dominate.

Community-led acquisition.

Professional creators are migrating their most engaged followers to owned communities: Discord servers, Slack channels, platform-specific community hubs. High-value peer-to-peer interaction within these spaces becomes the primary product and the main driver of retention.

Engagement in owned communities runs 8-10x higher than on public feeds (TagMango, 2025). The community generates word-of-mouth referrals, creating a localised viral loop that operates entirely outside traditional social media algorithms.

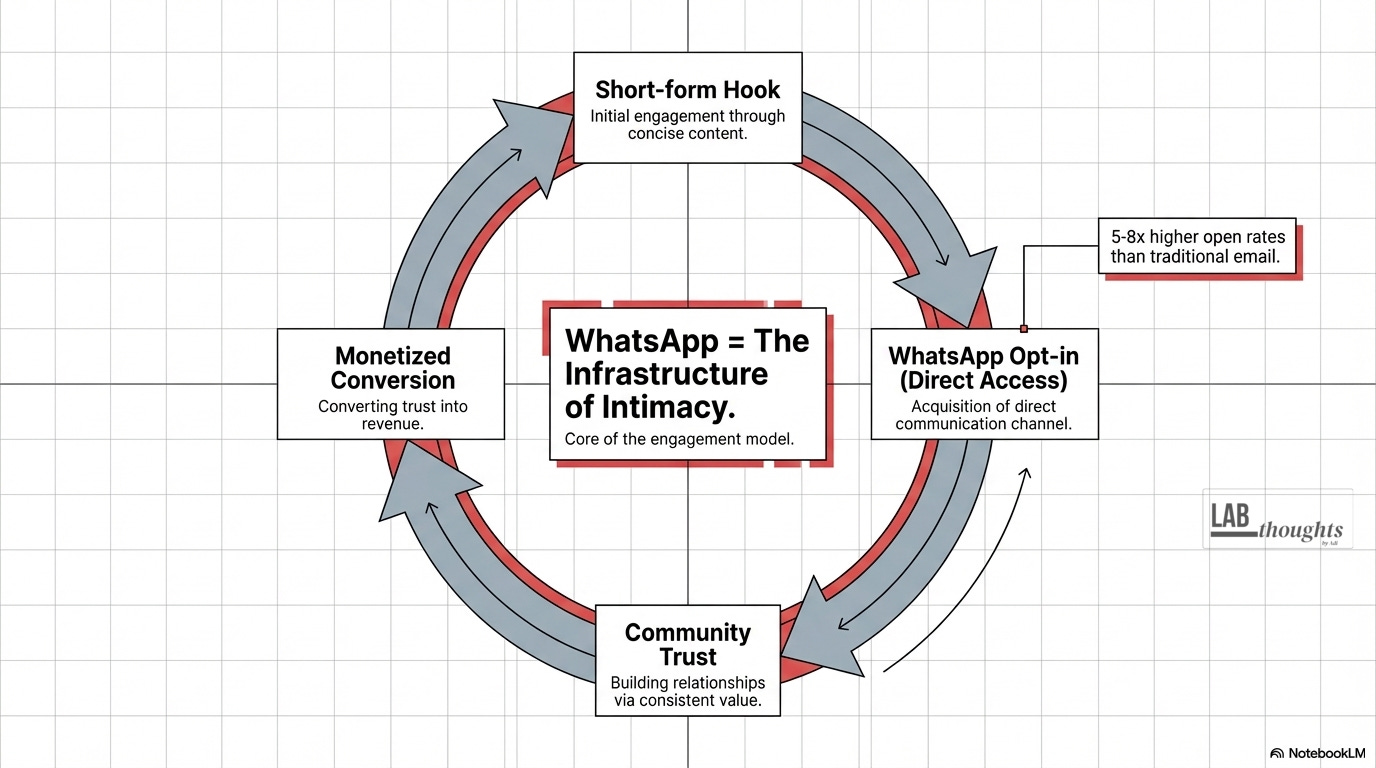

WhatsApp as distribution infrastructure.

In India, WhatsApp is not a messaging app. It is the fundamental infrastructure of digital intimacy and commerce.

Open rates run 5-8x higher than traditional email marketing. Professional creators offer a free, high-value lead magnet in exchange for a WhatsApp opt-in, moving audiences from rented algorithmic space to a direct-to-consumer channel.

Automated drip campaigns and community broadcasts, costing fractions of a rupee per message, create a reliable, high-conversion loop completely insulated from algorithmic policy shifts.

Funnel bridging and cross-pollination.

Two or more non-competing professionals in complementary niches, a corporate tax lawyer and a fractional CFO, for example, bundle their digital products and cross-sell to each other’s established audiences. The mechanism doubles or triples conversion potential with zero additional advertising spend, based on mutual authority transfer and shared trust.

For screen industry operators, the distribution loop mechanic is not new. It is the attention flywheel applied to a different asset class.

The principle is identical: own the audience relationship, reduce dependency on third-party distribution, and build compounding returns from each piece of content.

The difference in India is that WhatsApp functions as the primary “owned channel” in a way that has no Western equivalent. Anyone designing a distribution strategy for the Indian market who does not build WhatsApp into the loop is leaving the most powerful channel on the table.

The Bharat engine: Tier 2/3 vernacular scale

The professional creator pivot relies on sophisticated IP packaging and engineered distribution loops. But the sheer explosive scale of the Indian creator economy is being driven by something else entirely: a demographic and linguistic shift that most English-language industry analysis underestimates or ignores.

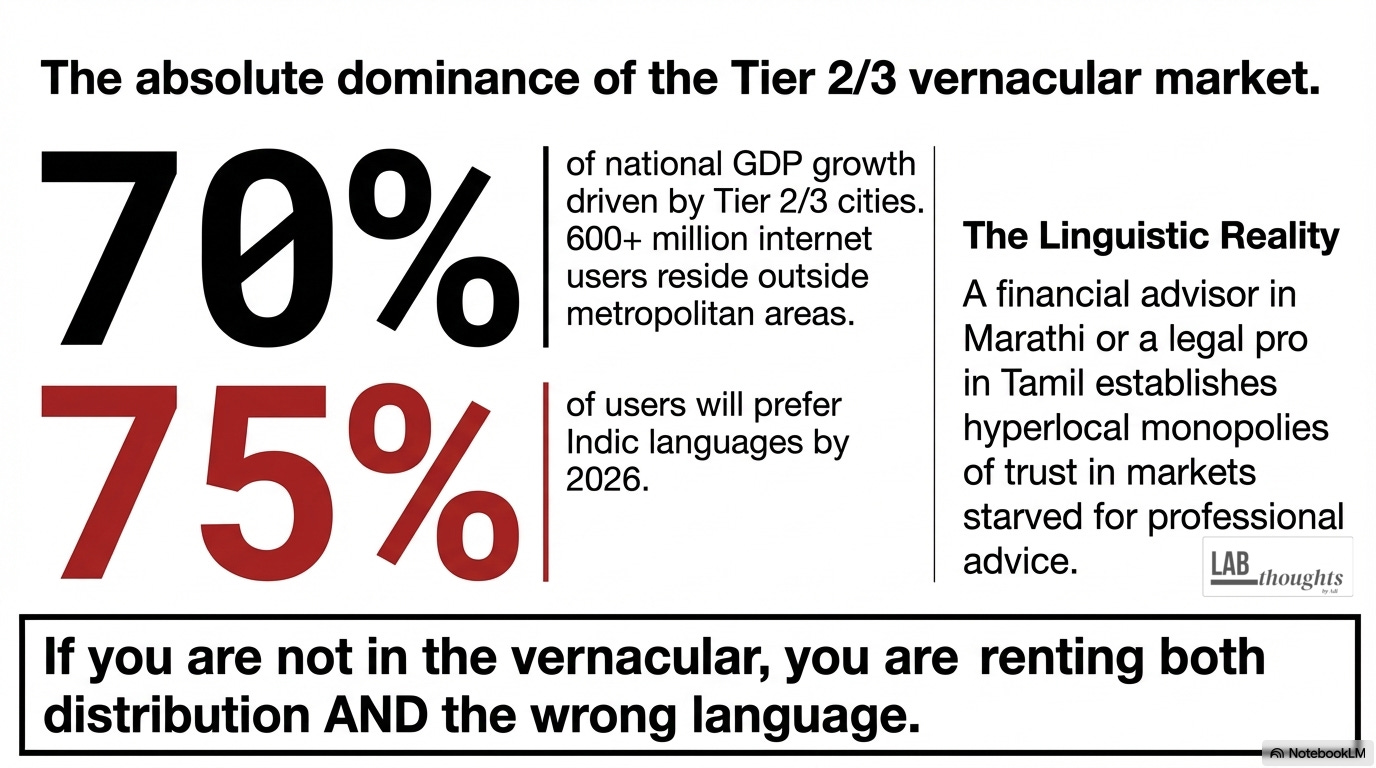

India had roughly 886 million internet users in 2024 (IAMAI-Kantar, 2024). Over 600 million of those reside outside metropolitan areas. Tier 2 and Tier 3 cities now contribute up to 65% of festive e-commerce orders, significantly outperforming metros in growth velocity (Market Xcel, 2025).

These cities are projected to drive 70% of national GDP. The professional creator who ignores Bharat does so at their own peril.

The linguistic landscape dictates the rules. India has over 1,600 spoken languages. By the end of 2026, more than 75% of Indian internet users are expected to consume content primarily in languages other than English.

The IAMAI-Kantar 2024 report indicates roughly 900 million users have accessed the internet in Indic languages, with a majority of urban users preferring Indic language content.

For the professional creator, this is not a localisation problem. It is a market dominance opportunity. A financial advisor explaining algorithmic trading in Marathi, or a legal professional detailing agricultural compliance laws in Tamil, is not merely translating content. They are establishing hyperlocal monopolies of trust in markets starved for high-quality professional advice.

Consumers in Tier 2/3 markets prioritise cultural alignment: 84% report it as a primary factor in purchasing decisions (The PR Post, 2025). Micro-influencers with localised followings yield engagement rates up to 8x higher than mega-influencers.

The platform dynamics reinforce the point. ShareChat reports 325-plus million MAUs, Moj at nearly 160 million MAUs. Josh describes 163 million users creating and consuming in local language.

WhatsApp has over 500 million users in India. Distribution loops in Tier 2/3 are often multi-hop and socially relayed, not purely algorithmic feed discovery.

The “rented land” metaphor applies twice over: you are renting distribution AND renting the wrong language.

For Lab Thoughts readers, the Bharat engine is the APAC tell. Vernacular-first, mobile-first, community-distributed content is not a niche Indian phenomenon.

It is the pattern that Southeast Asian markets are also following. Indonesia, the Philippines, Vietnam, these markets share the same structural conditions: massive mobile internet adoption, linguistic diversity, Tier 2/3 as the growth engine, messaging apps as distribution infrastructure.

India is running the experiment at the largest scale. The results will travel.

What this means for operators

The Indian creator economy professionalising is not a social media story for the marketing department. It is a structural shift in how expert-led content gets built, packaged, distributed, and monetised across APAC.

Here is what it means, depending on where you sit.

For brand content strategists and agency leads.

Stop buying creators. Buy distribution loops. The buying unit should be a packaged series plus a measurement plan, not a single post.

The data is clear: 73% of brands now prefer micro and mid-tier creators, 72% prefer long-term partnerships over episodic campaigns, and compensation models are shifting from flat fees to performance-based revenue share with strict sales attribution and CAC analysis (Dataslayer, 2025; Impact, 2025).

If you are still briefing one-off influencer posts with vanity metrics, you are funding someone else’s distribution loop without capturing any of the compounding value.

For producers and studio executives.

Treat India’s creator-to-IP pipeline as a development surface. The “Little Things” pathway, digital-first IP acquired by Netflix for later seasons, is a template, not an anomaly.

The Banijay Asia / Collective Artists Network announcement to build a “creator-centric universe” spanning long-form to micro-drama signals that studios are beginning to treat creator IP as a packageable, distributable asset class.

The question for development slates: are you scouting this pipeline, or are you waiting until someone else has already packaged the rights?

For talent managers and agencies.

Own the measurement layer or get commoditised. Talent agencies are moving from rented SaaS analytics to in-house tools and acquisitions to control data and prove ROI. If you do not own measurement, platforms and brands will set the terms.

Shift talent strategy from “faces” to “formats”: build rosters around repeatable IP formats with documented brand safety, audience, and conversion proof.

Watch this next

The Banijay Asia / Collective Artists Network move is a directional signal, not a proven pattern. But it is the studio-side confirmation that creator IP is being treated as an asset class, not a marketing channel.

Watch whether other studios follow, what rights structures they use (creator-friendly or extractive), and whether the Tier 2/3 vernacular opportunity gets built into the packaging or bolted on as an afterthought.

The broader signal: India’s creator economy professionalisation is running 3-5 years ahead of where comparable dynamics will land in Southeast Asia, the Middle East, and parts of Africa. APAC is the lab. India is the experiment at scale.

The operators who read the results first will set the terms.

If you found this useful, share it with one person who is making brand, rights, or distribution decisions in or around APAC.

If this raised a question about a project you are working on, email me at adi.tiwary08@gmail.com. I work with producers, development teams, and strategists on projects that need sharper positioning, stronger buyer legibility, or clearer rights strategy. The best place to start is a Project Audit.

Note: Market-sizing and ecosystem shift claims are supported by official or primary industry research. The “who wins” prediction and operator implications are reasoned analysis built on those dynamics and should be treated as informed inference, not provable fact. TagMango-sourced data is treated as directional given the platform’s commercial interest in the creator SaaS market.

Sources

Coherent Market Insights, “India Creator Economy Market Forecast, 2025-2032,” accessed February 2026

CRISIL Ratings, “Digital media scooped 46% of India’s ad spend,” 2025

Kotak Mutual Fund, “India’s Creator Economy: Growth, Trends & Influence 2025,” accessed February 2026

Exif Media, “The Creator Economy in India 2025: Trends, Earnings, and Opportunities,” accessed February 2026

IAMAI-Kantar, “The State of Digital in India 2024,” accessed February 2026

Silicon Valley Product Group, “Product vs. Project Teams,” svpg.com