At FilMart in Hong Kong in March 2026, COL Group and BeLive Holdings announced what they called “Microdrama in a Box.” The offer was clear: a white-label app stack bundling episodic playback, gamification, reward mechanics, AI subtitling, hybrid monetisation tools, and access to COL’s IP catalogue. A telco, broadcaster, or OTT platform with capital and a brand could, according to the pitch, be live in thirty days.

Timothy Oh, General Manager of COL Group International, put it directly: “We’re removing operational complexity for our partners.”

He was not wrong. That is exactly what the product does.

But there is a question sitting underneath the pitch that the thirty-day launch window does not answer. If a telco in Indonesia buys the box, and a broadcaster in the Philippines buys the same box, and a regional OTT in Vietnam buys the same box, all with overlapping catalogue and near-identical mechanics, what is the competitive position of any of them?

That is not a detail. It is the entire commercial decision. And it is not unique to buyers of white-label infrastructure. It applies to every operator entering, expanding, or repositioning in the micro-drama category right now: producers negotiating rights terms, brands commissioning pilots, investors doing diligence, platforms deciding what to build versus what to license.

The question is not whether micro-drama is a real business. It is. The question is which part of it you actually own, and whether the part you own compounds.

The business model is real. The operating system underneath it is what most people are missing.

In July 2025, a previous Lab Thoughts piece called Two-Minute Titans made the case that micro-drama is a serious commercial category. It is.

China’s micro-drama market generated approximately US$6.93 billion in revenue in 2024, surpassing domestic box office for the first time. Global in-app revenue from short-drama apps reached roughly US$700 million in Q1 2025 alone, up from US$178 million in the same quarter a year earlier. The US is the highest-ARPU market globally.

That piece argued the business model.

What it did not fully name is the operating system underneath it.

A business model describes how money flows. An operating system describes what the machine requires to run. You can replicate a business model at a surface level without understanding the system, but you will not get the same output, and the gap shows up exactly when it is most expensive: when you have already committed capital, rights, and time.

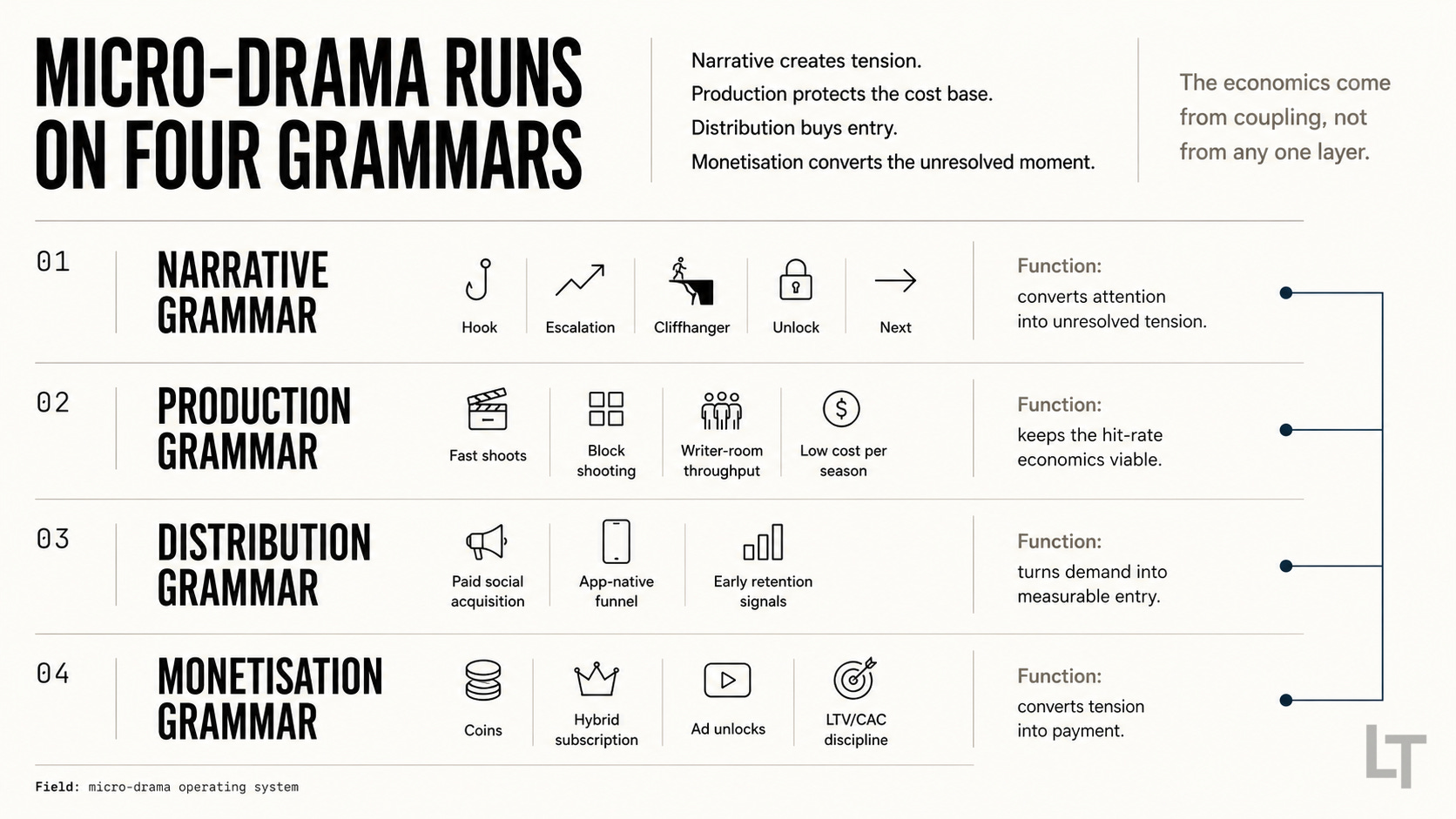

Micro-drama runs on four grammars. They are distinct, they interact, and none of them produces the category’s economics when built in isolation.

The first is the narrative grammar: 60 to 90 second vertical episodes, aggressive cliffhangers at the end of each one, legible archetypes established in the first five seconds, and seasons of 60 to 100 episodes architected as a single extended arc. The unit of storytelling here is not the episode. It is the loop: hook, escalation, cliffhanger, unlock, next. Everything that makes the format hold attention and convert attention into payment lives in that loop.

The second is the production grammar: 8 to 14 day shoots for full seasons at $150,000 to $300,000 per series, block shooting by location rather than episode order, 15 to 20 script pages per day, writer rooms generating 15 to 20 scripts per month. This is factory logic, not craft logic. The speed and the cost structure are not compromises. They are the economic condition that makes the format viable at the hit rates that actually prevail.

The third is the distribution grammar: app-native funnels where 70 to 80 percent of installs come from paid social advertising, not organic discovery; sequential release architecture calibrated to build binge velocity; recommendation systems optimised on first-five-episode retention, not aggregate watch-time. Social platforms are the acquisition channel. The dedicated app is where monetisation happens. The two are not interchangeable.

The fourth is the monetisation grammar: coin-based in-app purchases, hybrid subscription tiers, ad-supported unlocks for price-sensitive segments, and unit economics borrowed from free-to-play mobile gaming rather than from streaming. The target is a roughly 3:1 LTV/CAC ratio.

The profitability of a series becomes visible within 48 to 72 hours of launch. The paywall is not a friction point imposed on a story. When the narrative grammar is designed correctly, the paywall is a narrative moment. The viewer is at maximum emotional investment precisely when they are asked to pay.

That last sentence is the coupling in one sentence.

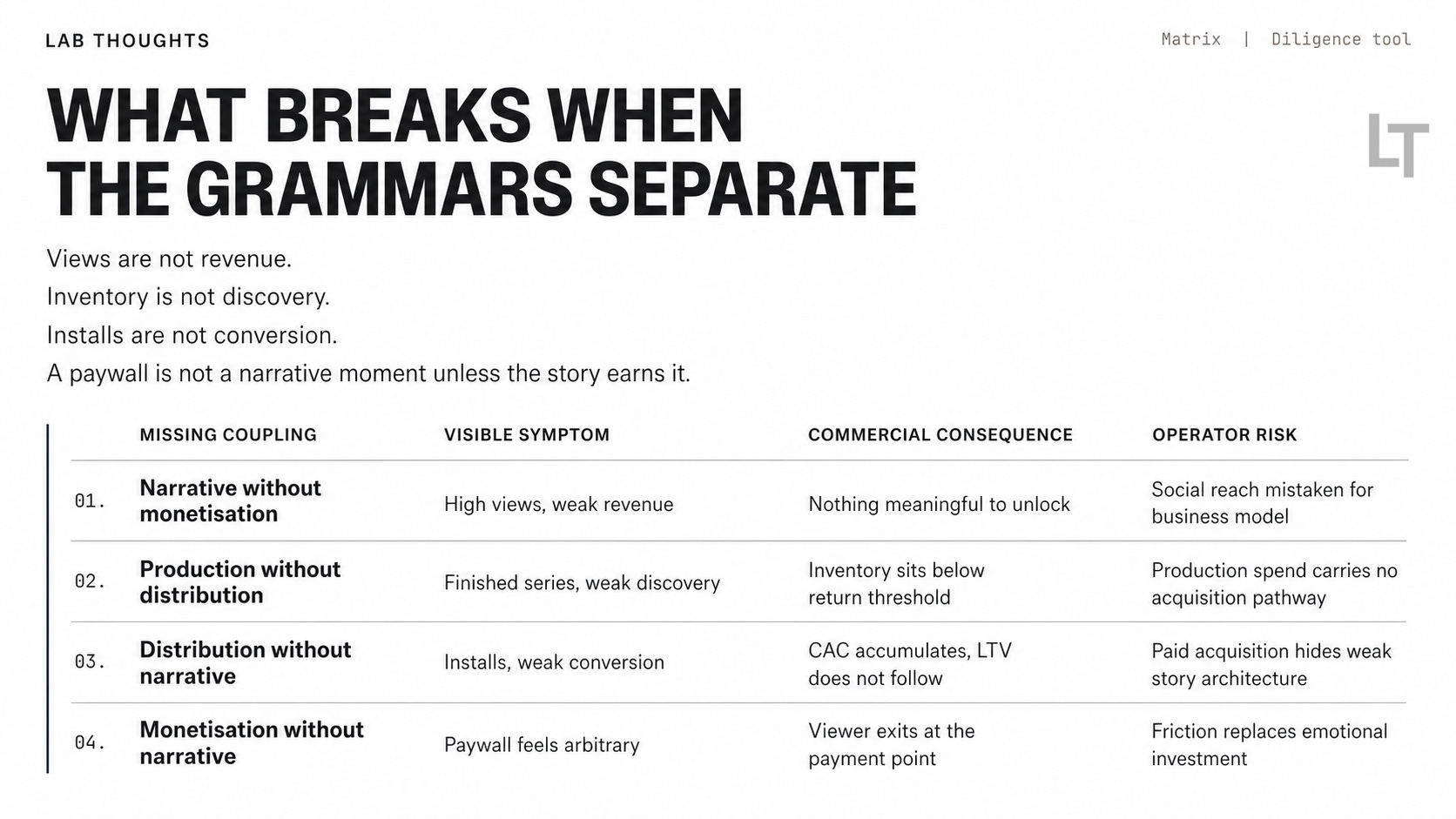

Why coupling is the whole point

Each grammar has value on its own. The compounding economics come from designing all four together, not from assembling them after the fact.

When the narrative grammar runs without the monetisation grammar, you get a vertical series with high views and no revenue. The audience has no reason to pay because the story gave them nothing to unlock. Free, resolved cliffhangers on TikTok are the clearest version of this. Plenty of brands and creators have made technically competent vertical content that behaved exactly like a social clip series and converted at zero.

When the production grammar runs without the distribution grammar, you get a well-made series that no one finds. In this format, discovery does not happen through app store search or algorithmic recommendation from a standing library. It happens through paid social advertising. Investing $300,000 in production without a User Acquisition (UA) budget and a funnel into a dedicated app produces content that sits at whatever level the creator’s existing social reach can sustain. That is rarely the level that generates a return on the production cost.

When the distribution grammar runs without the narrative architecture, you get an app with a catalogue that cannot hold anyone past the free episodes. The coin system only activates when the viewer is at maximum narrative investment. That investment is not automatic. It is designed, at the episode level, through the cliffhanger. A platform with strong acquisition mechanics and weak narrative grammar acquires users it cannot convert. CAC accumulates. LTV does not follow.

When the monetisation grammar runs without the narrative design that earns it, you get a paywall that reads as a wall. The viewer has not been brought to a point of unresolved tension. The payment request is arbitrary. Most people leave. The ones who stay do so despite the mechanics, not because of them.

The Chinese operators who built the category correctly in its first phase owned all four grammars inside integrated structures: IP pipelines, production infrastructure, distribution apps, and monetisation systems built to fit the story architecture. That is why the unit economics in the Chinese domestic market are the benchmark. They were not assembled from parts. They were designed as a system.

2026 is when the grammars came apart

Three moves in the first quarter of 2026 mark a structural phase change.

The COL and BeLive “Microdrama in a Box” stack makes production infrastructure inputs, distribution player technology, and monetisation mechanics purchasable in a single transaction. A regional buyer no longer needs to build any of those three grammars from scratch. The box handles them.

Rising Joy’s co-branding and co-creation partnership with Malaysia’s Double Vision provides a second model: curated IP library, format bibles, music clearances, and localisation capability, licensed to a regional broadcaster that brings local production relationships and market access. Two grammars acquired via partnership, with the other two supplied by the buyer’s own organisation.

COL Group’s own FlareFlow platform is scaling to 180 original micro-drama series in 2026, running more than 400 creative experiments per month on hook types and cliffhanger formats. At that volume, narrative grammar is no longer a creative act. It is an R&D function with an industrialised testing pipeline.

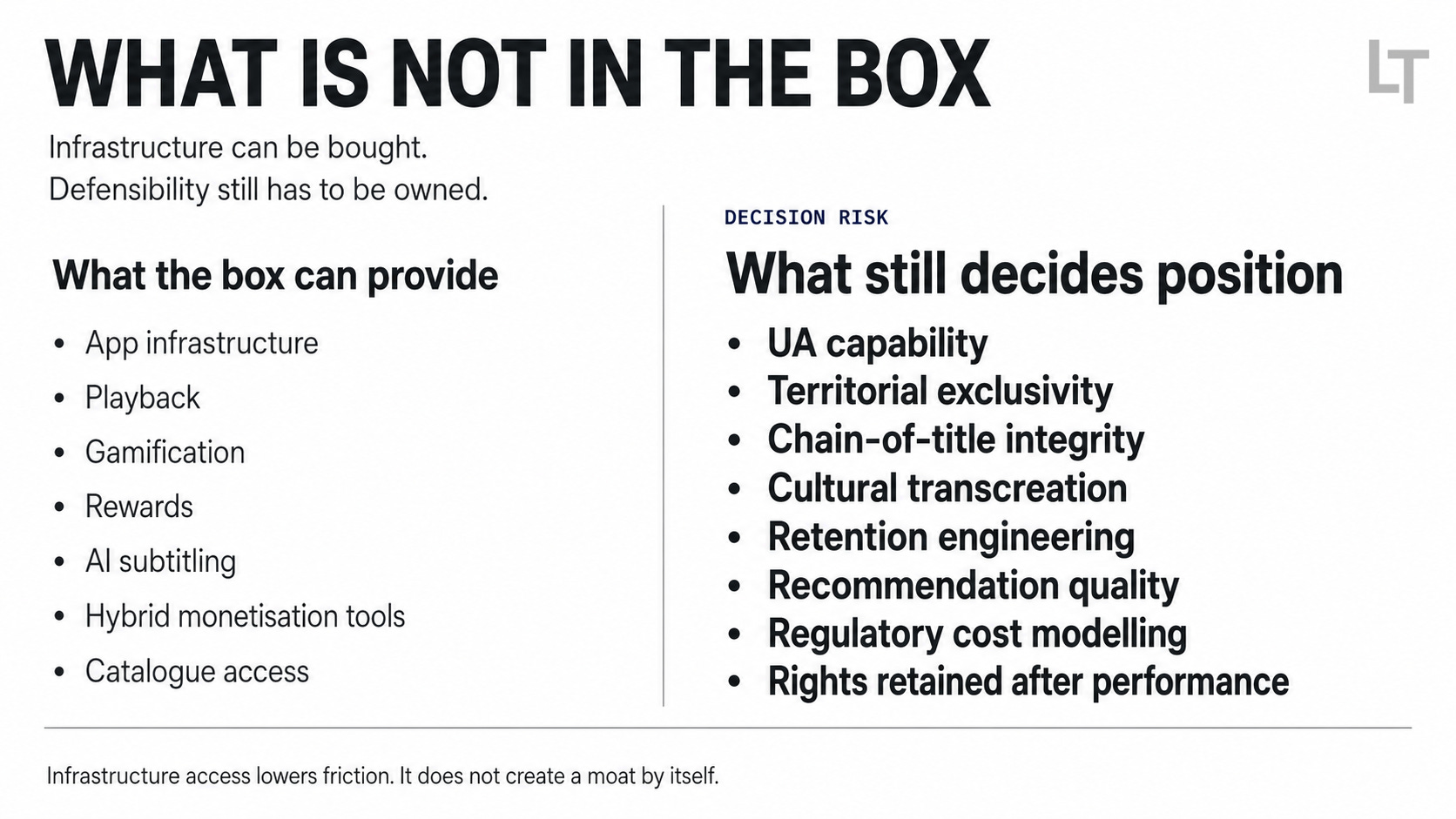

Together, these moves confirm what has been building since late 2024: the barrier to accessing three of the four grammars has dropped significantly. Technology, catalogue, and basic monetisation tools are now off the shelf at a price point most serious regional operators can reach.

What is not in the box: UA capability, territorial exclusivity, chain-of-title integrity, and cultural transcreation.

UA capability is worth pausing on. In the format as it currently operates, 70 to 80 percent of installs are driven by paid social advertising. That is not a marketing line item. It is a structural requirement of how audiences discover and enter the format. A platform that launches on white-label infrastructure without a sophisticated paid social capability has distribution mechanics without distribution. Acquisition costs in this category rose 40 to 60 percent between 2023 and 2025. The operators with durable positions are those who have figured out how to bring CAC down as the category matures, not those who bought access to the UA channel at peak cost.

Cultural transcreation is the second gap that subtitling tools do not close. AI handles language. It does not handle romance codes, family hierarchy, class signals, shame lines, or the specific pacing preferences that vary between Indonesia and the Philippines and Thailand and Vietnam. A catalogue that feels like translated Chinese product rather than locally resonant content will find a ceiling on retention that no amount of gamification mechanics can move.

The regulatory overlay lands in the same window and is not priced into most entry models.

The EU AI Act reaches full application on 2 August 2026. Under Article 50, any video, audio, or text generated by AI must carry machine-readable labelling. Deepfake content must be disclosed to the audience, even in creative works. Imperceptible watermarking is required to survive compression and cropping. Third-party verification interfaces must be available. This is not a future compliance question for platforms operating in European markets or targeting European users. It is a 2026 cost that changes per-conversion economics.

The Australian Competition and Consumer Commission’s 2026-27 enforcement priorities name subscription traps, dark patterns, false urgency pricing, and influencer disclosures explicitly in digital markets. The AANA Code of Ethics governs advertising conduct. For any platform or brand operating in or distributing into Australia, these are live regulatory requirements that affect how monetisation mechanics can be designed and disclosed.

The structural consequence is not that the infrastructure phase is bad news for the category. Shopify was not bad news for commerce. But Shopify made clear that owning a store was not the same as owning a business. The infrastructure phase in micro-drama makes the same distinction visible, at scale, across a category that is moving fast enough that operators can commit significant capital before that distinction becomes apparent.

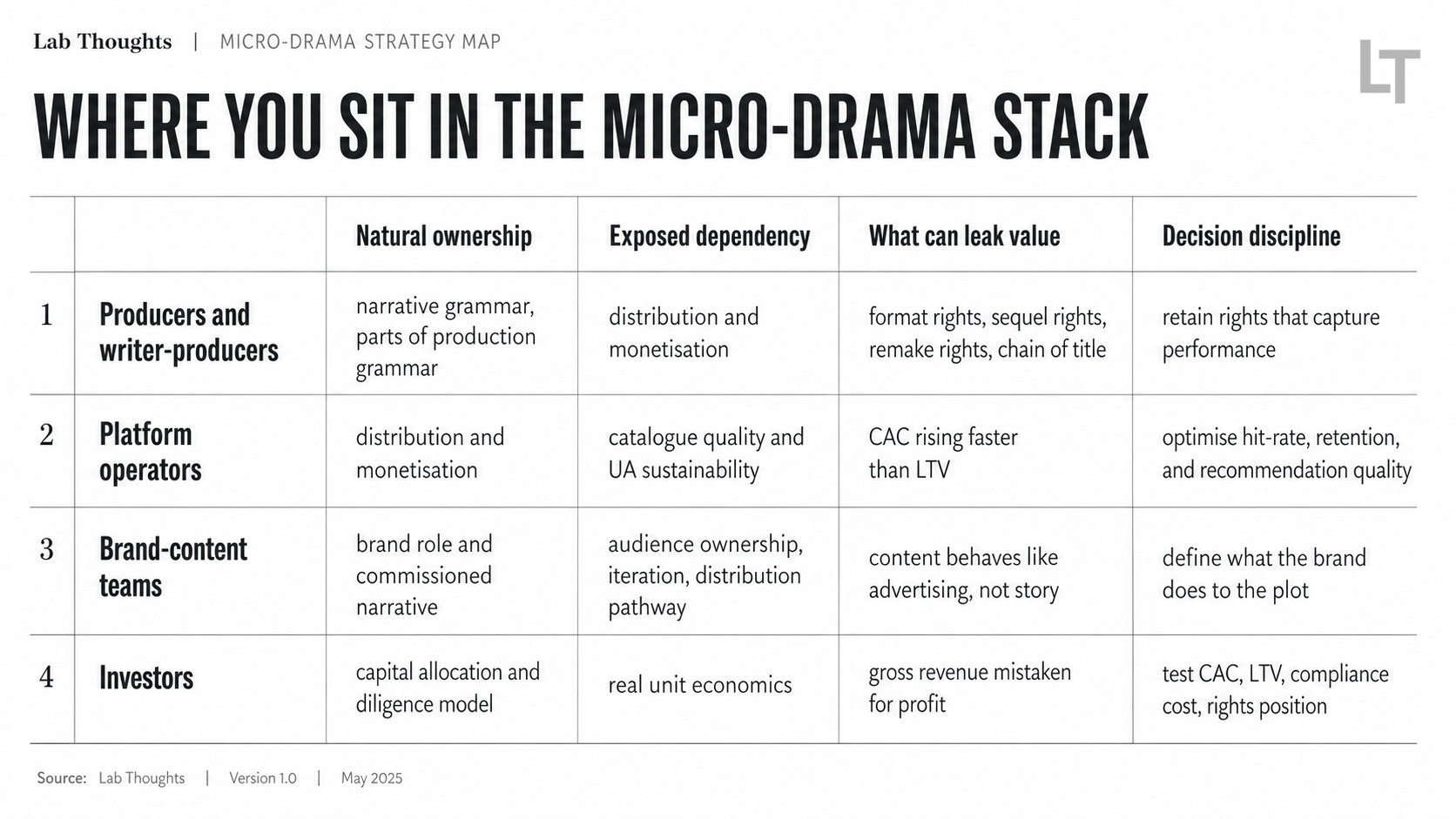

Where you actually sit in the stack

The coupling problem presents differently depending on which role you occupy.

For producers and writer-producers, the natural ownership position is the narrative grammar and parts of the production grammar. The format fluency, the writer room, the block-shoot discipline, the world and character IP. The coupling pressure lands through distribution and monetisation, which most platform deals absorb in exchange for reach. The producer delivers two grammars. The platform takes the other two. What the producer is left with depends entirely on what they retained in the deal.

Indian remake rights for Korean micro-drama formats increased in value by 85 percent in recent years, according to industry data. The reverse-licensing play, using a vertical run as a proof of concept to sell a longer-form series, is now a documented commercial strategy rather than a theoretical one. That leverage only exists if the producer retained the adaptation rights that make it possible. Long-form rights, sequel rights, and format rights given away at the commissioning stage are not recoverable after the title performs.

There is also a chain-of-title problem specific to the format’s production speed. Fast-moving crews routinely fail to secure proper releases for music, locations, or secondary literary material. AI-generated scripts or visual sequences may not be protectable under US copyright law, which makes the underlying asset legally fragile at exactly the moment it becomes commercially valuable. A micro-drama library without a clean chain of title is not an asset. It is a liability waiting for scale to trigger it.

For platform operators and platform investors, the natural ownership position is the distribution and monetisation grammars. The pressure lands through catalogue quality and UA sustainability. As white-label stacks commoditise the infrastructure layer, the platform’s differentiation narrows to hit-rate and UA discipline. Catalogue volume is not a moat. Catalogue quality ratio is.

DramaBox, one of the stronger independent performers in the category, reported approximately US$323 million in revenue and approximately US$10 million in profit in 2024. That is a roughly 3 percent net margin on a revenue base that requires continuous UA reinvestment to sustain. When CAC rises and hit-rate holds flat, that margin disappears. The platforms with durable positions are building retention engineering and recommendation quality, not just catalogue size.

For brand content teams, the coupling pressure is specific: most brand entries into micro-drama acquire one grammar, narrative via commissioning, and rent or ignore the other three. The result is content that cannot be iterated on, an audience the brand does not own, and metrics that cannot be connected to business outcomes because the distribution and monetisation layers belong to whoever the brand placed the content with.

The Chinese beauty brands that generated the category’s most cited commercial results, Kans and Proya, did not place advertising into existing micro-drama series. They built series in which the brand’s narrative role was the mechanism of the story. Kans ran five series alongside influencer Jiang17. The reported result was over 3.34 billion yuan in attributed sales and 50 billion views. The mechanism was not product placement. It was that the brand’s product changed what the characters were able to do in the plot. Remove the brand, the story stops working. That is the test.

A brand that cannot answer in one sentence what it does to the plot, not what it says in the plot, has not commissioned a story. It has commissioned a well-produced advertisement that will be correctly identified as such in the comments section.

For investors doing diligence on micro-drama plays, the coupling problem shows up as a framework mismatch. Traditional film and television diligence frameworks do not produce accurate reads on a format whose economics are closer to free-to-play mobile gaming than to SVOD. Gross revenue presented without UA spend netted out is not profit. CAC trajectory is more predictive of a platform’s position in three years than content library size. Regulatory compliance costs as of August 2026 are inside the unit economics model, not beside it.

APAC is where the pattern breaks show up first

The reason APAC is the right lens for this category is not that it is Adi Tiwary’s home region. It is that APAC is where each grammar is being stress-tested against real market conditions, in real time, before equivalent tests run in Western markets.

China built the template by vertically integrating all four grammars inside single corporate structures from the start. Douyin, Kuaishou, and COL Group held IP pipeline, production infrastructure, distribution rails, and monetisation in coupled systems. The US$6.93 billion domestic revenue figure is the output of that coupling, not of any single grammar.

Southeast Asia is where decoupling is being tested live. The primary buyer market for COL and BeLive is Indonesian telcos, Philippine broadcasters, Vietnamese OTT players, and their counterparts across the region. Sensor Tower data reported a 61 percent quarter-on-quarter increase in SEA short-drama app downloads in Q1 2025. The demand is real.

What these markets lack is the UA capability, the cultural transcreation layer, and the rights infrastructure to convert that demand into durable business positions. They are buying two grammars and operating under the assumption that the other two will follow. The results over the next 18 months are the most important real-time evidence in the category about whether “Microdrama in a Box” builds businesses or produces a generation of commodity apps.

India is the hybrid monetisation laboratory. Full-price In-App Purchase does not clear. The viable model is freemium with low-cost coin increments alongside advertising. What India is generating is evidence about which grammar combinations are necessary and sufficient in high-volume, price-sensitive markets. That evidence is commercially relevant anywhere the demand-side economics look similar.

Australia is a regulated distribution territory, not a natural production hub for the format at current scale. Its significance is regulatory. The ACCC’s 2026-27 enforcement priorities, the AANA Code requirements, and the regulatory treatment of subscription mechanics and influencer disclosures in Australian digital markets are arriving 12 to 24 months ahead of equivalent enforcement pressure in most Southeast Asian markets. Operators and advisers reading Australian regulatory signals are looking at a preview of what compliance will cost across APAC by 2028.

The questions that do real work

Before any new commitment in this category, five questions are worth sitting with. They do not require long answers. They require honest ones.

Which of the four grammars does this deal or strategy actually give me ownership of, and which am I renting? What does renting cost me if the title or platform hits scale?

If this project performs, which rights do I hold that let me capture that performance? If the platform makes that decision, I do not hold them.

If a competitor in my territory launches the same infrastructure stack with the same catalogue next quarter, what is my actual differentiation? If the answer is “our brand,” that is a marketing problem, not a grammar.

Can I state in one sentence what the brand does to the plot, not what it says in the plot?

Which of my 2026 regulatory obligations are inside my current cost model, and which are not?

What this adds to the thread

This essay, and the Lab Thoughts micro-drama thread it sits in, is built on a working argument that micro-drama is an operating system, not a content trend or a distribution format.

Two-Minute Titans argued that the business model is real. The Microdrama in a Box field note identified the infrastructure phase transition. This essay tries to name the coupling logic that makes both of those observations matter commercially.

A practical operating resource for brands commissioning their first vertical series is coming shortly. Watch for it.

If you are sitting with a version of this problem on a live project and want a clear outside read before more time goes into the wrong direction, send a short note describing the situation to adi.tiwary08@gmail.com. I take a small number of these each quarter.