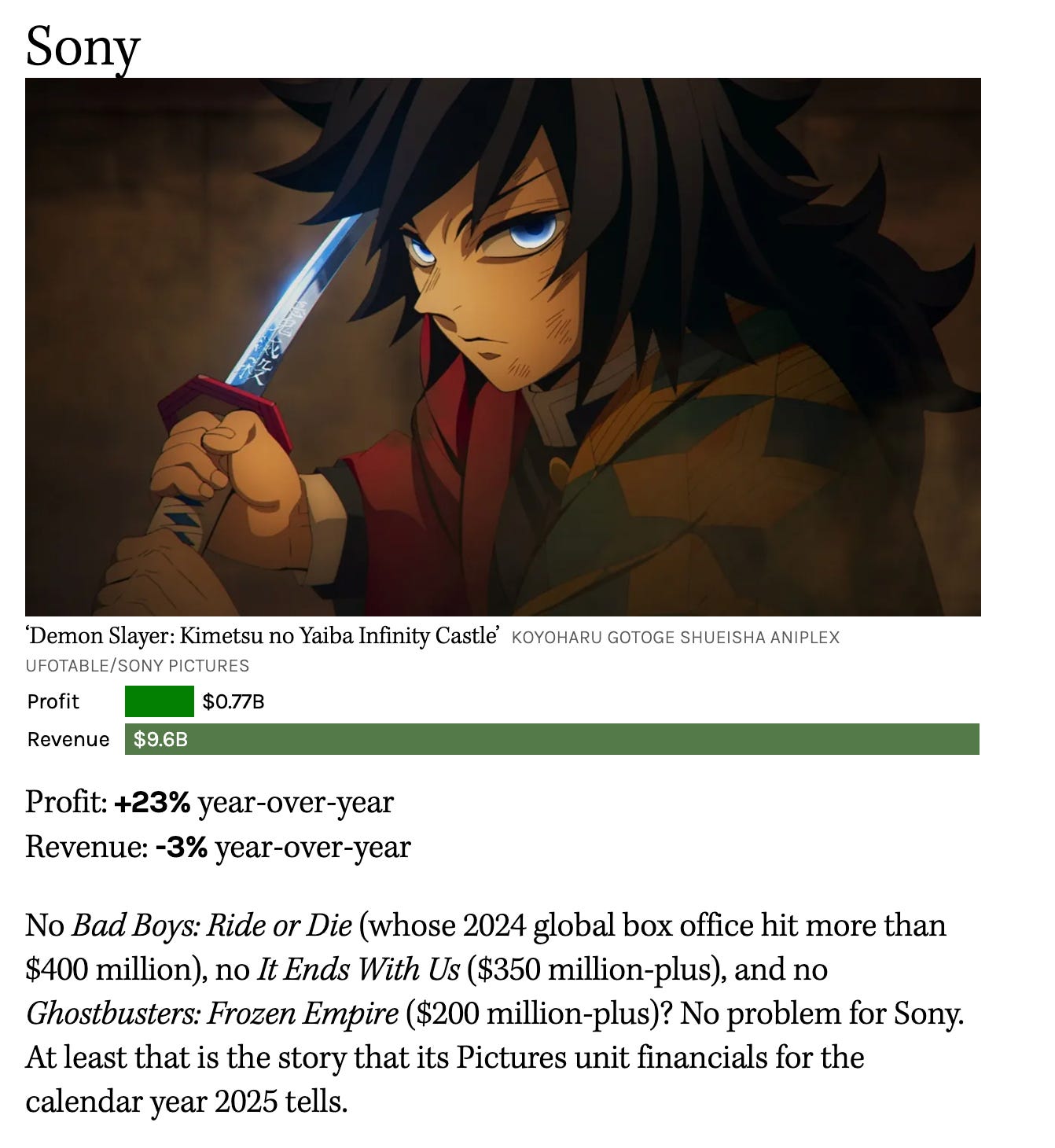

Sony Pictures made more money in 2025 than it did in 2024. Its box office revenue fell by a third.

That outcome got a paragraph in most roundups. I think it deserves considerably more than that.

Sony grew profit 23% on revenue that declined 3%.

No Bad Boys. No It Ends With Us. No Ghostbusters sequel doing quiet work in the background. A theatrical slate that produced $1.5 billion globally, down from $2.4 billion the year before. And yet: more money, not less.

The industry’s reflex, when a studio’s box office falls sharply, is to look for what went wrong. That reflex is leading most people to misread the most instructive studio result of the year.

Sony did not have a down year rescued by ancillary income. It had a year that revealed what its business actually is, now that the blockbuster safety net was removed. The structure held. And the reason it held is that Sony, somewhere along the way, stopped trying to be Disney.

What “not trying to be Disney” actually means

Disney’s model is built on IP ownership at civilisational scale. Marvel, Star Wars, Pixar, Disney Animation, ESPN. The strategy is total cultural saturation across every demographic, every format, every window, every theme park queue in the world.

It works, spectacularly, for Disney. It is also completely unreplicable by any other studio operating on earth today.

This should be obvious. It is apparently not, because the entire legacy studio industry has spent the better part of a decade trying to construct a version of it. Warner Bros. alone is simultaneously rebooting DC, reviving Harry Potter as a television franchise, and betting that Minecraft can anchor a new generation of IP. Everyone is hunting for the flywheel.

Sony looked at that race and opted out. Whether that was strategic clarity or structural necessity is, by now, an irrelevant question. The results are the same either way.

Instead, Sony built three things that are now paying out simultaneously.

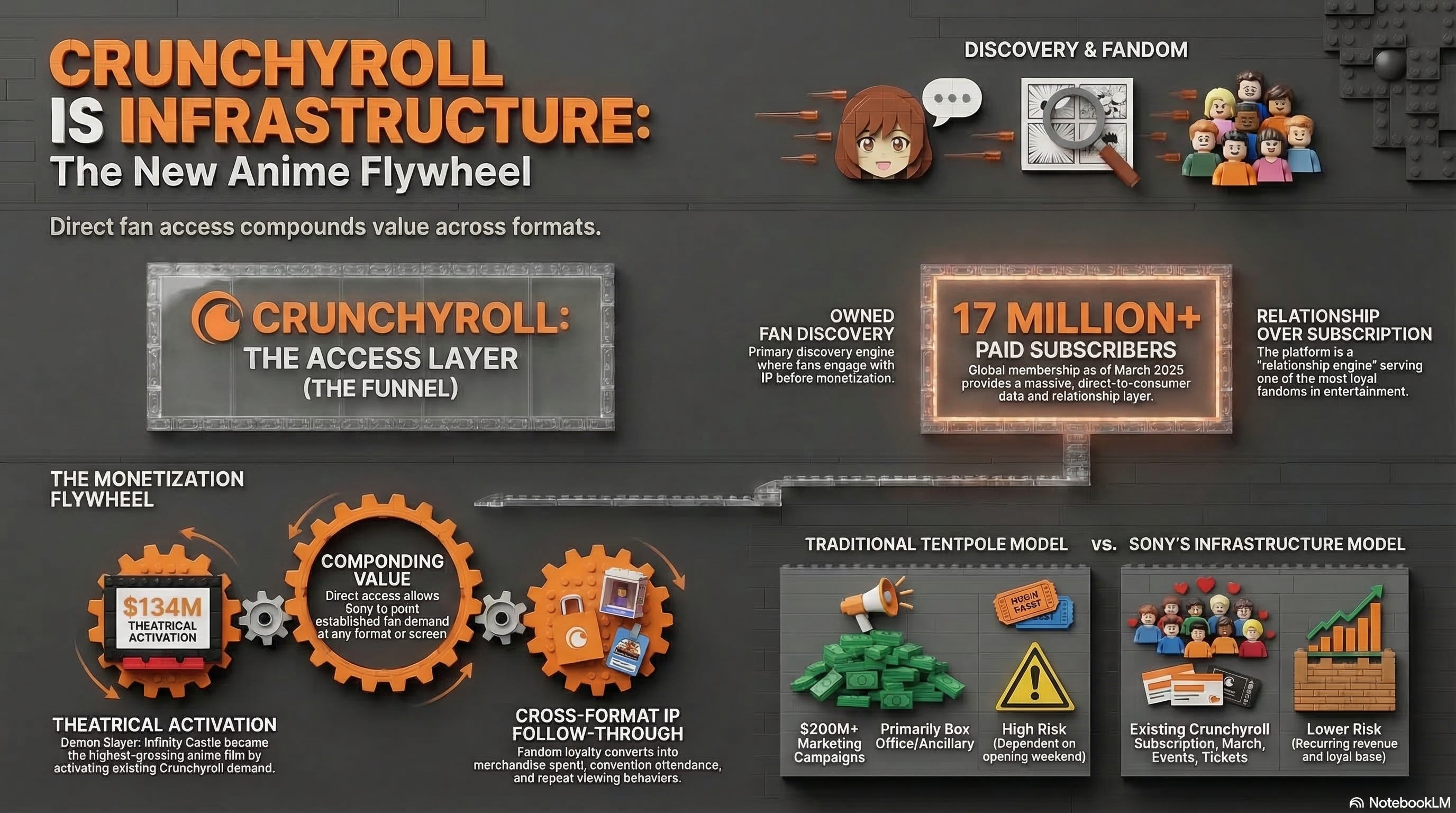

Bet one: Crunchyroll is not a side business

When Sony acquired Crunchyroll in 2021 for just over a billion dollars, the deal was treated as a niche play. Anime was a passionate but bounded fandom. The acquisition made sense as a library move. It was not, the conventional wisdom suggested, a strategic pivot.

That reading was wrong.

Crunchyroll now has tens of millions of subscribers globally. It is the dominant anime streaming platform in the English-speaking world and a significant player across Southeast Asia, Latin America, and Europe. Its subscriber base did not stop growing in 2025. It quietly underwrote a year in which Sony’s theatrical revenue fell sharply.

More importantly, Crunchyroll is not just a streaming service. It is a direct-to-consumer relationship with one of the most commercially loyal fandoms in entertainment. Anime fans track release schedules, buy merchandise, attend theatrical events, and follow IP across formats with a commitment that most western studio marketing departments would spend enormous sums trying to manufacture.

That loyalty is not created by a campaign. It accumulates over years of consistent fandom servicing. Sony bought the infrastructure that holds it.

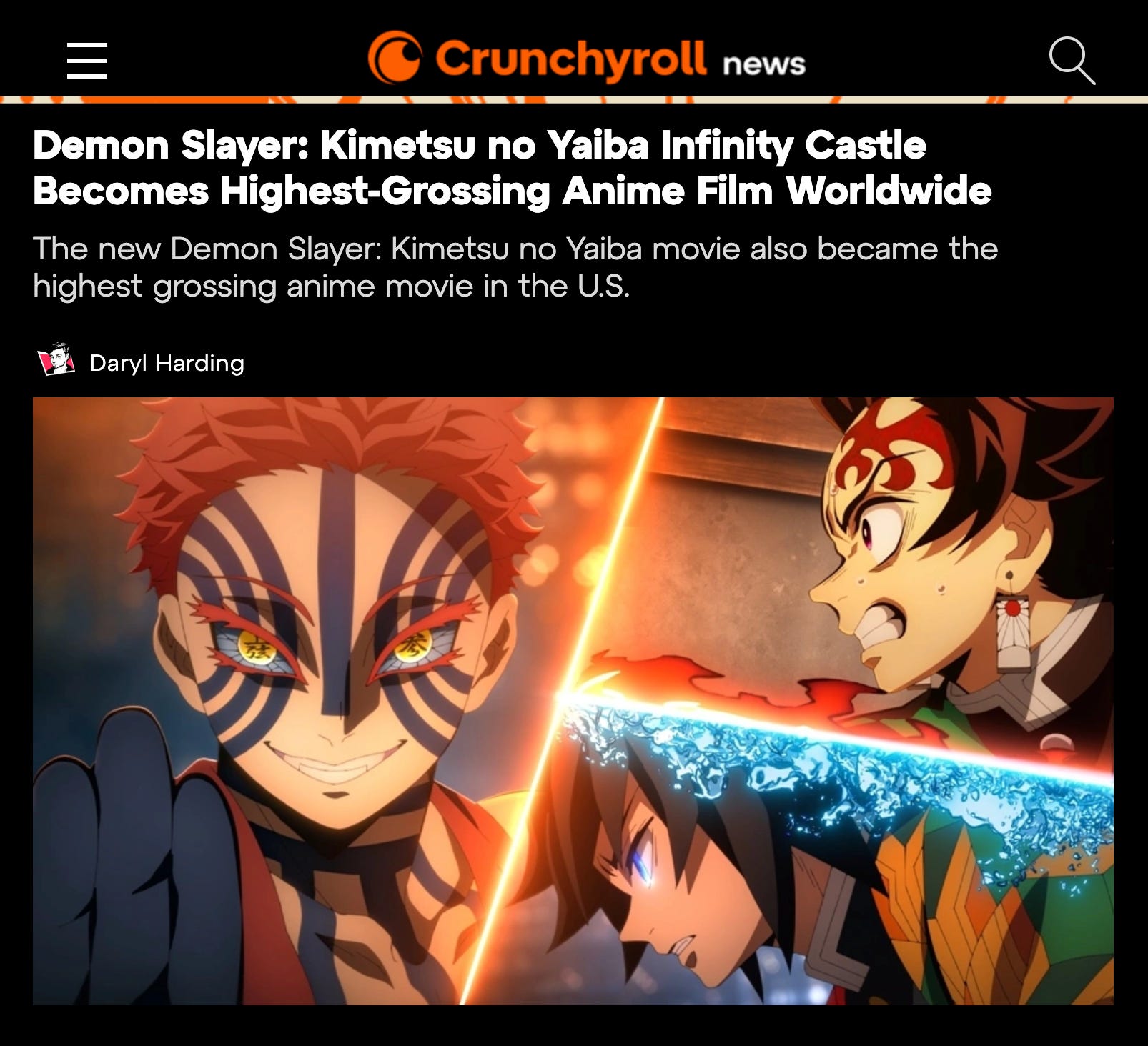

Demon Slayer: Infinity Castle is the clearest illustration of what happens when that relationship is activated theatrically. The film grossed $134 million in 2025 and became the highest-grossing anime film of all time globally.

Sony did not create that demand. It inherited it, cultivated it through Crunchyroll, and then pointed it at a cinema screen.

That is a fundamentally different business model than spending $200 million on a tentpole and hoping the marketing campaign does its job in three weeks.

Bet two: local-language film as portfolio, not charity

The industry’s relationship with local-language production has always been complicated. The major studios maintain local operations in key markets, but the films they produce are rarely treated as commercially central. They are positioned as regulatory compliance, relationship maintenance, or modest revenue diversification. Not the thing the studio president leads with on an earnings call.

Sony leads with them.

The evidence is not just that Sony made local films in 2025. It is what those films did commercially and what they generated downstream.

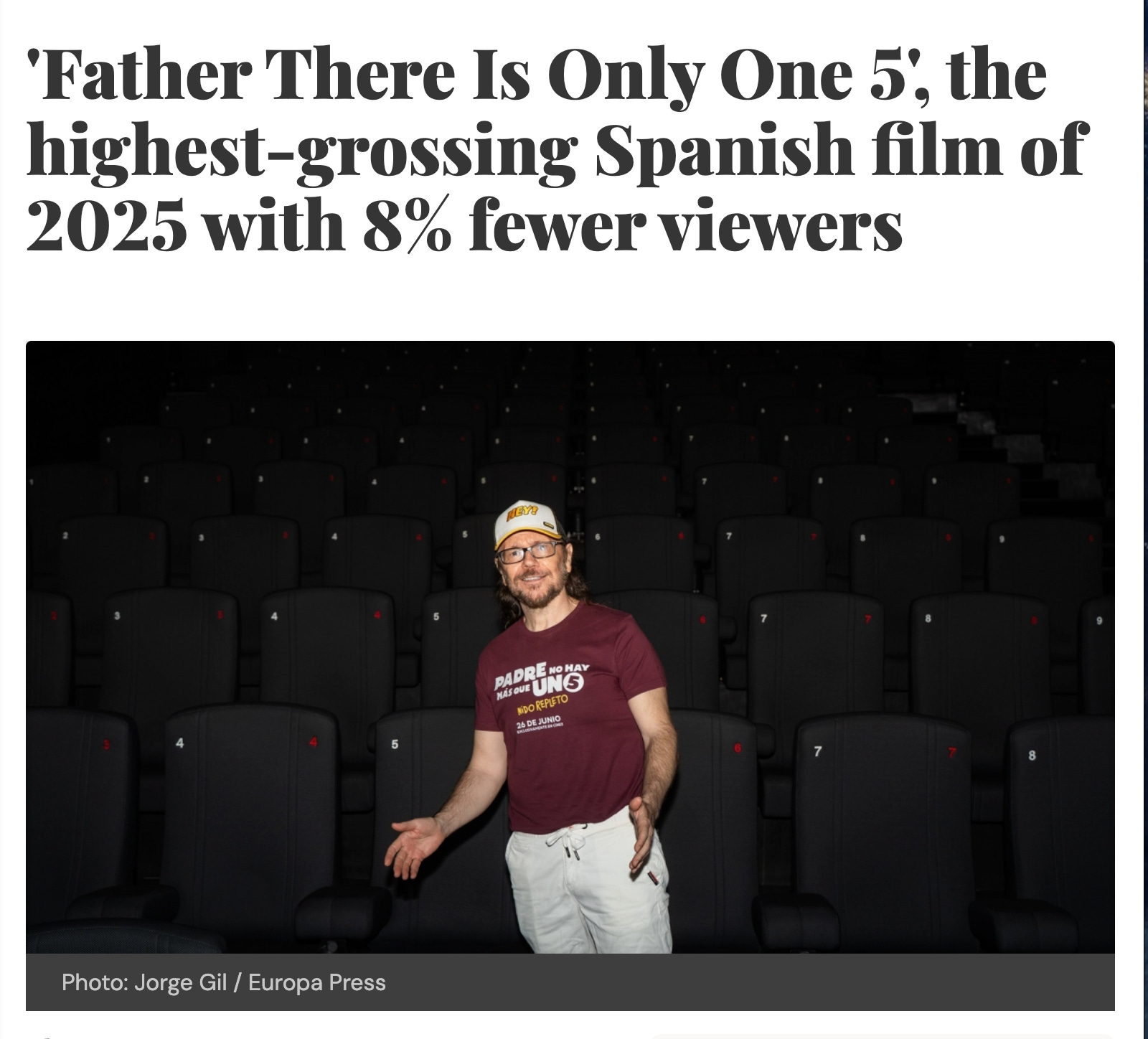

In Spain,Father There Is Only One 5 (Padre no hay más que uno 5: Nido repleto), a domestic family comedy distributed by Sony, was the highest-grossing Spanish film of the year, earning approximately €13 million theatrically before moving to Netflix five months later.

That theatrical run generated enough commercial heat that a third party, Prime Video and Atresmedia, subsequently announced a television series continuation. Sony distributed the film. It did not need to own the series to have its distribution investment validated by what the franchise became.

In Germany, The Three Investigators: Carpathian Dog grossed nearly $13 million worldwide, drawn entirely from a book and audiobook franchise with over 75 million units in circulation across those two formats in Germany alone.

Sony did not build that fandom. It built a production and distribution operation capable of activating it theatrically. The sequel is already scheduled.

These are not vanity projects subsidising goodwill in local markets. They are commercially oriented productions made for audiences that are already there, requiring no four-quadrant global marketing spend to find their viewers. The economics are structurally different from the tentpole model. The risk profile is too.

Most of Sony’s competitors understand this in principle. Few have the operational commitment to treat it as core business rather than a footnote to the slate.

Bet three: format neutrality as strategic discipline

Sony does not own a major streaming platform. For years this was treated as a competitive liability. Sony was the studio without a home, selling content to whoever was buying, dependent on third parties to reach audiences.

Now in 2026, that liability looks like a structural advantage.

Sony is not subsidising a streaming service that needs to justify subscriber numbers every quarter, not caught between a theatrical windowing strategy and the needs of a direct-to-consumer platform that wants content immediately, and not making programming decisions to satisfy an algorithm rather than an audience.

It sells to Netflix, to Apple TV+, to Amazon, to whoever values the content most at the moment of sale. That means Sony’s content is priced by the market rather than by internal transfer pricing, and Sony has maintained relationships across the entire buyer landscape rather than structural dependence on one.

The Spanish franchise result illustrates this in miniature. Sony distributed a film theatrically. Netflix picked it up for streaming. A third party commissioned the series. At no point did Sony need to own the platform to extract value from the IP chain it had activated.

That is not an accident of circumstance. It is what format neutrality delivers when it is applied as discipline rather than treated as a reactive fallback.

What this means if you are building IP in this part of the world

Sony’s model will not translate directly to an Australian or Southeast Asian producer. The scale is different. The infrastructure is different. The starting position is different.

But the underlying logic looks far less abstract once you look at what actually happened across APAC in 2025.

The Sony thesis, fandom depth over mass breadth, portfolio economics over blockbuster dependence, buyer optionality over platform captivity, shows up in three distinct regional forms.

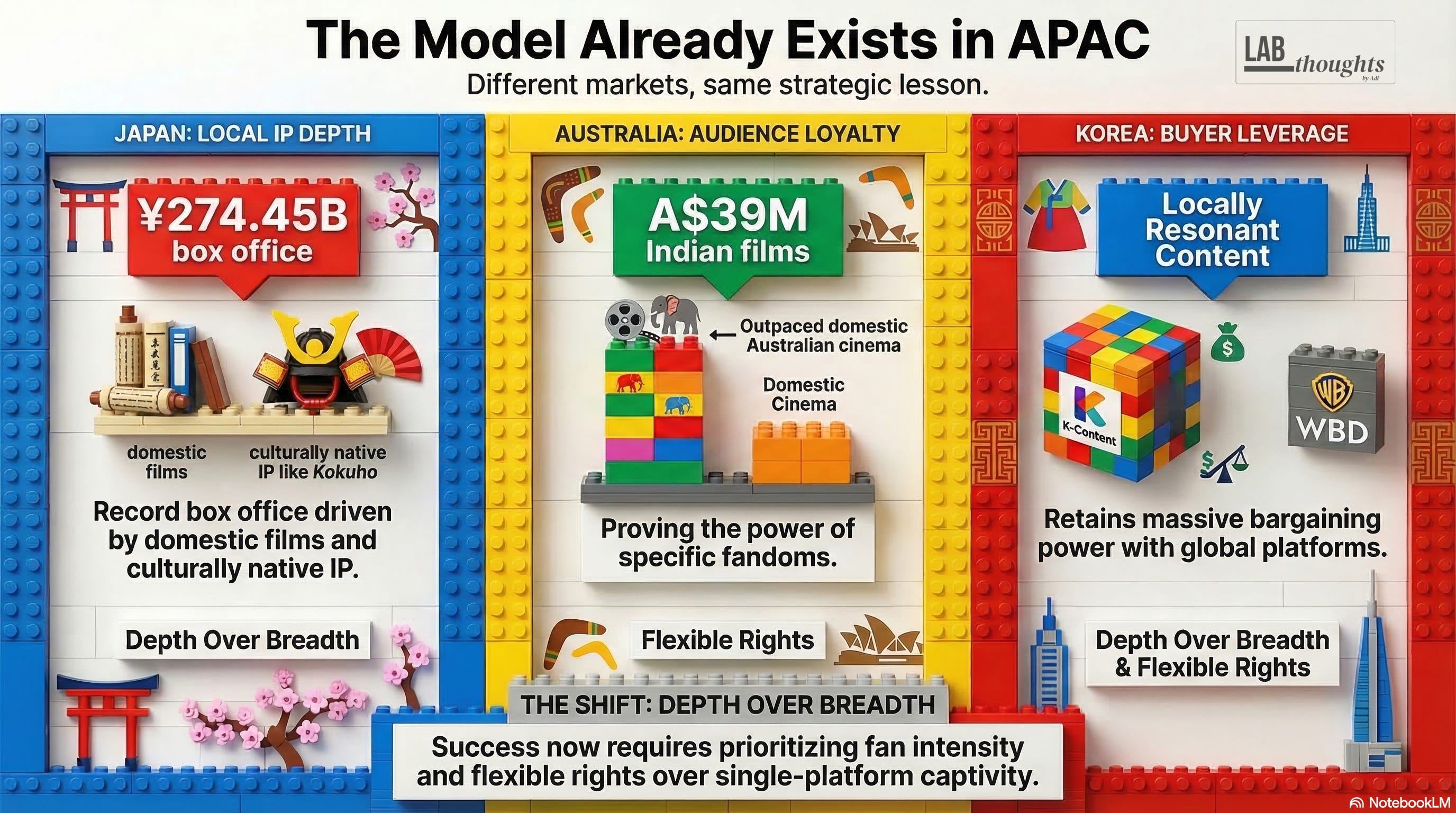

In Japan, the box office hit a record ¥274.45 billion in 2025, up 32.6% year on year, according to the Motion Picture Producers Association of Japan. Domestic films drove ¥207.57 billion of that total. Local titles accounted for seven of the top ten releases.

Demon Slayer led, but the more telling result was Kokuho, a nearly three-hour kabuki drama that became the highest-grossing Japanese live-action film ever released domestically.

That is not a market being carried by imported tentpole logic. It is a market demonstrating that culturally native IP, backed by fan intensity and repeat viewing behaviour, generates serious economic weight entirely on its own terms.

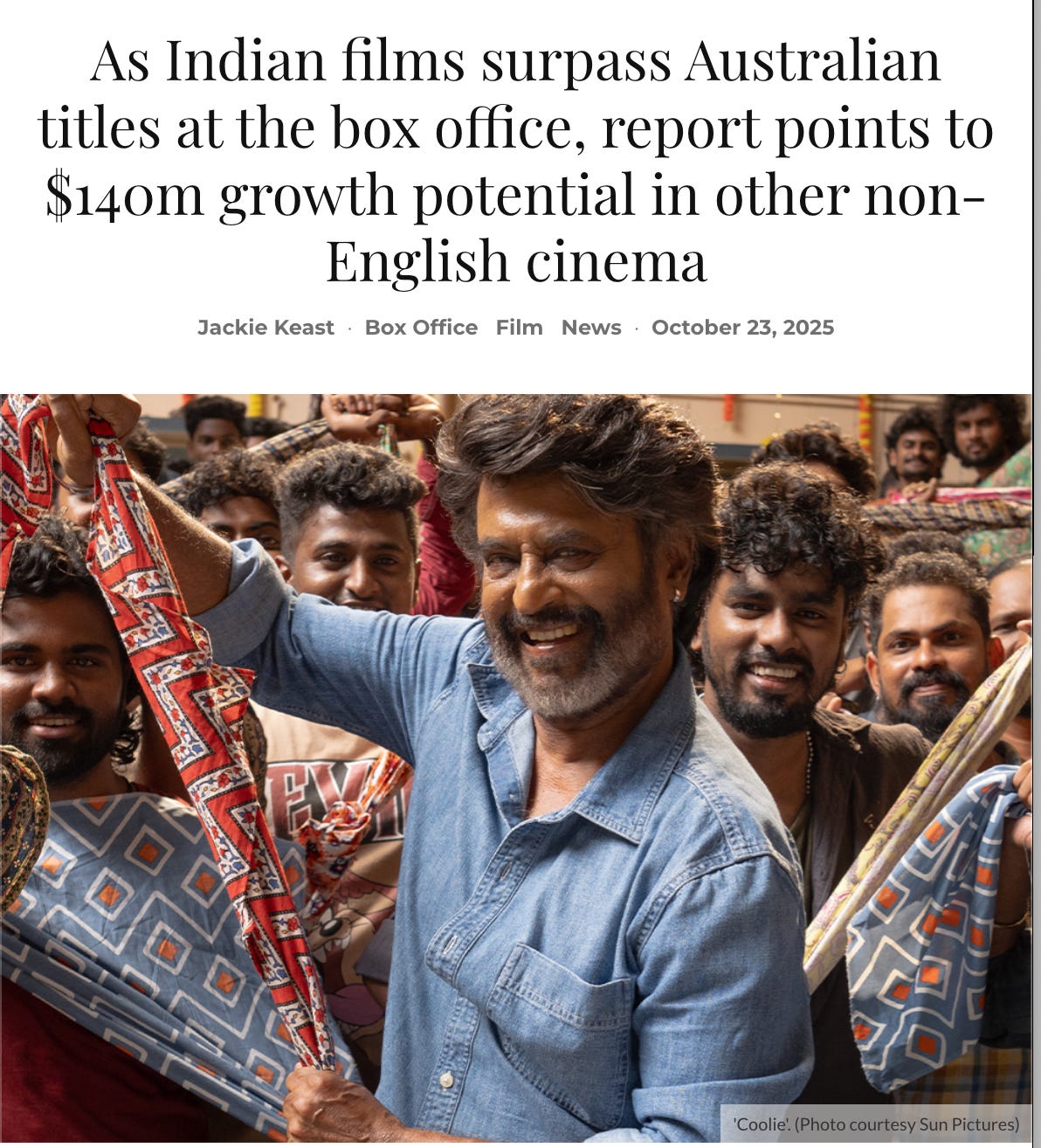

Australia offers a different version of the same argument. Indian films are now the third-largest box office force in the country after the US and UK, grossing A$123 million across 2023 to 2025 against A$74 million for Australian films over the same period. In 2025 alone, Indian titles were projected to pass A$39 million locally.

That is not a diaspora anecdote. It is evidence that culturally specific audiences with genuine loyalty create durable theatrical value without pretending to be four-quadrant mainstream product.

South Korea shows the third dimension. In October 2025, Warner Bros. Discovery and CJ ENM announced a multi-year partnership spanning exclusive K-drama premieres, a TVING hub on HBO Max across 17 APAC markets, and co-investment in new Korean drama for global distribution.

The significant detail is not the deal structure. It is that locally resonant Korean IP retained sufficient leverage to attract a major global platform partner on terms that kept the Korean side commercially relevant. The value travelled because the IP was not captive to any single buyer.

Put together, those three examples make the regional lesson harder to dismiss. Most producers in APAC are not failing to become Disney.

They are operating in markets where the smarter play increasingly looks like fandom depth over mass breadth, portfolio economics over blockbuster dependence, and flexible rights structures over single-platform captivity.

That is the part of Sony’s 2025 result that should travel.

The honest question

The standard ambition for anyone building an entertainment business outside the American major studio system is still framed as: how do we compete with Disney?

It is the wrong question. The right one is: why are we still organising our ambitions around a model designed for a different era, in a different market, by companies with structural advantages we do not have and cannot acquire?

Sony did not answer that question by accident. It answered it by being clear-eyed about what it is, what it is not, and where it can win without pretending to be something it isn’t.

That clarity is rarer in this industry than it should be.

If this raised a question about a project you are working on, email me at adi.tiwary08@gmail.com. I work with producers, development teams, and strategists on projects that need sharper positioning, stronger buyer legibility, or clearer rights strategy. The best place to start is a Project Audit.