A producer uploads a low-budget pilot to an open platform and waits.

Not for reviews. Not for awards chatter…and definitely not for a commissioner’s call.

They are waiting for retention, comments, shares, completion rate, clips cut by strangers, the first signs that an audience is doing the work a commissioner used to do in private rooms.

For most of the last decade, scripted development began with a greenlight. Now increasingly, it begins with proof.

That is the shift.

And it is why the YouTube versus Netflix framing misses the point.

The real question is not which platform is bigger. It is when money moves, who carries risk before it does, and what a producer gives up once it arrives.

The prototype nobody called a model

So in the early 2010s, a small group of Indian producers started making scripted shows for YouTube. TVF came first. Then Pocket Aces, with Dice Media producing Little Things, a low-budget relationship drama that found a real audience on YouTube before Netflix came in to acquire the later seasons.

No broadcaster greenlit any of it. No streamer wrote a development cheque. The producers moved anyway, patching the economics together with brand deals, YouTube ad revenue, and the willingness to carry the risk themselves until audience proof existed.

At the time, this looked like necessity as there were no other options. What it actually was, in retrospect, was a working prototype of the funding logic that now has $100 billion behind it.

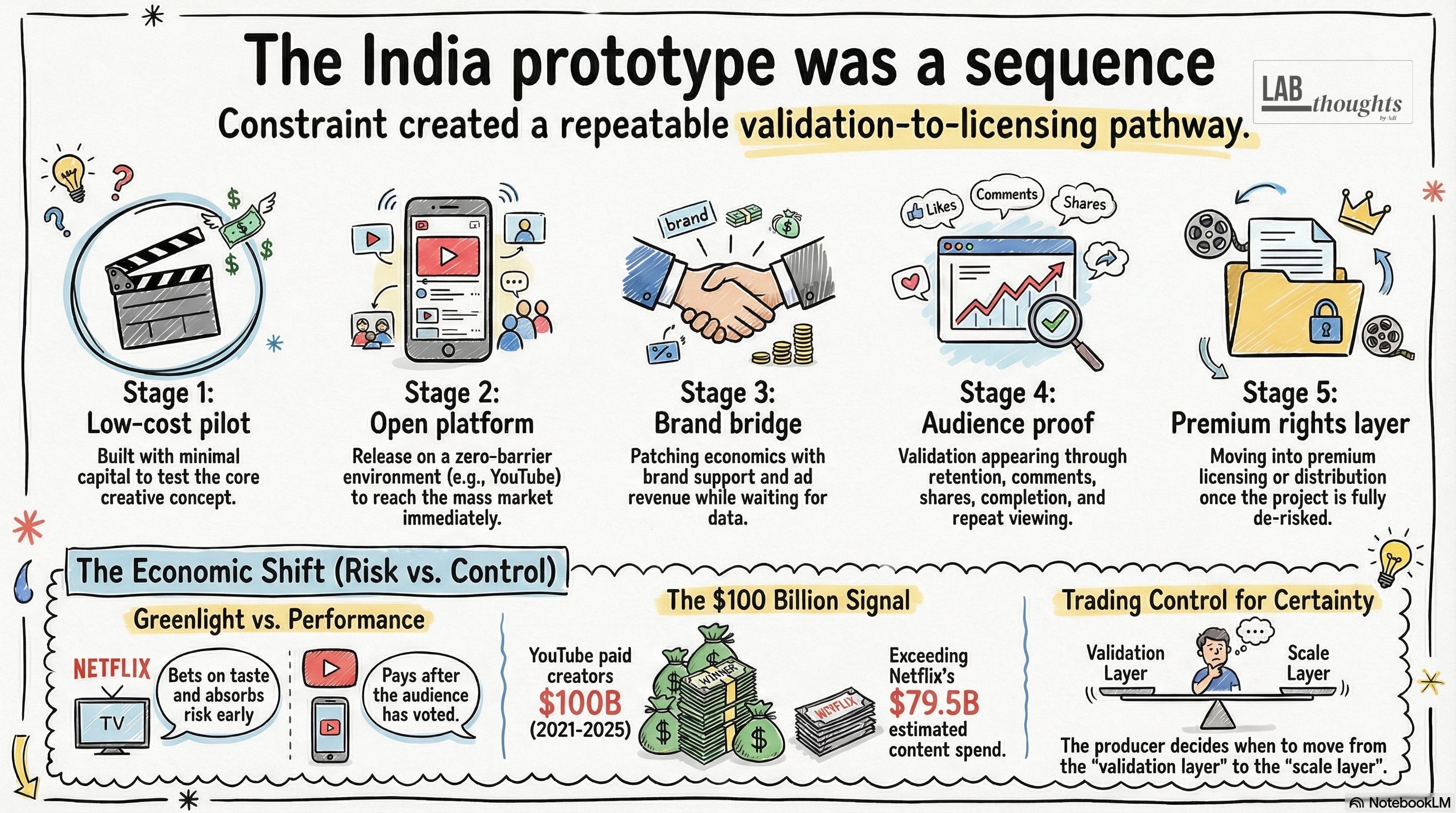

$100 billion, the number that reframes the argument

YouTube paid out more than $100 billion to creators, artists, and media companies between 2021 and 2025.

Netflix’s estimated cash content spend over the same period was $79.5 billion.

Most coverage treated this as a size comparison. It is not. It is a description of two completely different theories about when money should move and who should carry risk in the meantime.

Netflix writes the cheque before the audience exists. It bets on taste, absorbs development risk, and takes IP control as the price of that bet.

YouTube pays after the audience has already voted with their time. Creators and producers carry the early risk. The platform pays on performance, at scale, once demand is proven.

Neither model is better in the abstract. They are optimised for different kinds of operators at different stages of a project’s life.

The question worth asking is not which platform is winning. It is what each model requires of the people working inside it.

The India sequence

The TVF and Dice Media examples are not nostalgia. They are the clearest evidence available of what the performance-first funding logic actually produces when it works.

The sequence ran like this. Build on YouTube with minimal capital. Use brand partnerships to fill the gap that commissioners left open. Prove audience demand on an open platform. Then move into a more conventional licensing environment once the show has de-risked itself.

YouTube functioned as the validation layer. Netflix entered as the scale and premium-rights layer.

I think this model was not planned. It emerged from constraint and became legible as strategy only after it worked.

The India performance layer now has real capital in it. At WAVES 2025, YouTube’s CEO Neal Mohan stated that YouTube had paid more than INR 21,000 crore (USD 2.5-2.6) to Indian creators, artists, and media companies over the previous three years, with a further INR 850 crore (USD 100-105 million) of investment committed going forward.

That is not abstract creator economy rhetoric. It is a capital pool sitting outside the conventional commissioner system, available to producers willing to take audience risk first.

The most recent signal is Amazon MX Player’s launch of Fatafat in March 2026, reported by Deadline. A dedicated vertical for short-form, mobile-first scripted content, built on rapid consumption and ad-supported reach.

A mainstream platform building product architecture around this behaviour rather than treating short-form narrative as a sideshow.

The sequence is directionally right, but it is not structurally stable. Fatafat is a product bet, not a proven monetisation engine.

YouTube’s India payouts are real but heavily concentrated among the top of the creator distribution curve.

The TVF era worked partly because the producers were patient enough to wait, and because brand money existed to fill the gap. None of those conditions are guaranteed to replicate cleanly.

The pattern is legible. The economics are still being worked out.

What the producer is actually deciding

This is not a story about YouTube versus Netflix. The platform rivalry framing, which Ted Sarandos opened and YouTube’s own executives engaged with at Series Mania in March 2026, is a surface narrative. It obscures the more consequential shift.

The real shift is structural. For most of the past decade, the dominant funding logic in scripted content was: find a commissioner, get a greenlight, begin. The commissioner absorbed early risk. The producer traded control, and often IP, for that certainty.

What the India sequence shows, and what YouTube’s payout figures make concrete, is that a second logic now has enough capital behind it to function as a genuine alternative.

Build on an open platform. Carry the early risk. Prove demand. Then decide whether to move into a licensing environment or stay in the performance layer.

YouTube is not replacing the commissioner. It is changing the moment at which a producer has to decide whether they want one.

The question is not which model is better. It is at what stage of a specific project you want to trade control for certainty. That is a harder question than it looks, and the answer is different for every project.

APAC is where that question is being answered in real time. India has already produced the prototype. The short-form infrastructure is now being built at scale across the region.

ReelShort’s multi-year APAC expansion partnership with Hong Kong-based Asia Productions, announced in early 2026, is one signal among several that the region is becoming the primary testing ground for performance-led narrative models.

I think what gets resolved here will define the funding logic for mobile-first scripted content globally.

Why?

Because APAC is the lab.

So heres the open question

The producers who built TVF and Dice Media did not have a theory. They had no other option, and they moved.

The producers working now have both options available, with real capital sitting in each. That is a different and harder position to be in. Having a choice means having to make one.

At what stage do you want to trade control for certainty?

If this raised a question about a project you are working on, email me. adi.tiwary08@gmail.com

SourcesVariety, March 2026. YouTube managing director Justine Ryst, Series Mania fireside chat. YouTube $100 billion creator payout figure (2021–2025). Netflix $79.5 billion cash content spend comparison.

WAVES 2025. Neal Mohan, YouTube CEO. YouTube India payout: INR 21,000 crore over three years. Forward investment commitment: INR 850 crore.

Deadline, March 2026. Amazon MX Player launches Fatafat microdrama service in India.

Variety, March 2026. YouTube managing director Justine Ryst, Series Mania fireside chat. YouTube $100 billion creator payout figure (2021–2025). Netflix $79.5 billion cash content spend comparison.

WAVES 2025. Neal Mohan, YouTube CEO. YouTube India payout: INR 21,000 crore over three years. Forward investment commitment: INR 850 crore.

Deadline, March 2026. Amazon MX Player launches Fatafat microdrama service in India.